When it comes to managing property in the UK, there is more to it than simply finding reliable tenants and arranging maintenance. The financial backend of property management has not evolved at the same pace as legislative changes, tougher tax rules, and rising operating costs. As a result, strong financial management has now become the real engine of long-term property success.

If you’re a private landlord with a single buy-to-let, the estate agent managing a wide-ranging portfolio for clients, or an institutional investor building up a large-scale development called build-to-rent, one discipline will keep your finances in prime condition: property management accounting.

This comprehensive guide covers all of the aspects of navigating the monetary landscape of the United Kingdom real estate market, ensuring compliance, optimising earnings, and streamlining day-to-day financial routines.

Quick Brief: Who This Guide Is For and Why It Matters

This guide is explicitly tailored for:

- UK Private Landlords: Seeking to maximise allowable expenses, keep their cash flows clean, and submit self-assessment tax returns with ease. If you are registering for self-assessment for the first time, our guide on Online Tax Return Registration for First-Time UK Taxpayers can help.

- Estate and Letting Agents: Opening and closing hundreds of rentals per day, ensuring legal compliance with strict regulatory bodies, and holding client monies securely.

- Property Investors & Developers: Minimising losses on their growing portfolios through a focus on yield, capital growth, depreciation, and corporate structuring. Learn more about how depreciation affects financial reporting in our practical UK depreciation accounting guide.

Why Property Management Accounting Matters

In property, it’s cash that’s king, but it’s data that’s the crown. Problems with your property finances don’t simply mean that you don’t have good financial visibility; they can also mean that you get a hefty fine and HMRC visits, unpaid tax bills, tax bill errors and loss of reputation. Smart accounting turns your financial records from a history book into a forward-looking strategic plan—so you’ll never overpay on tax or lose a pound of rental income.

What Is Property Management Accounting?

Property management accounting is essentially a specific type of accounting that concerns only the income, expenses, capital investments, and financial obligations of a real estate asset.

Unique issues with recurring rental cycles, tenant deposit protection, client-allocated funds, service charges, ground rents and property-specific capital allowances are the aspects of property accounting that are unique to the general business accounting.

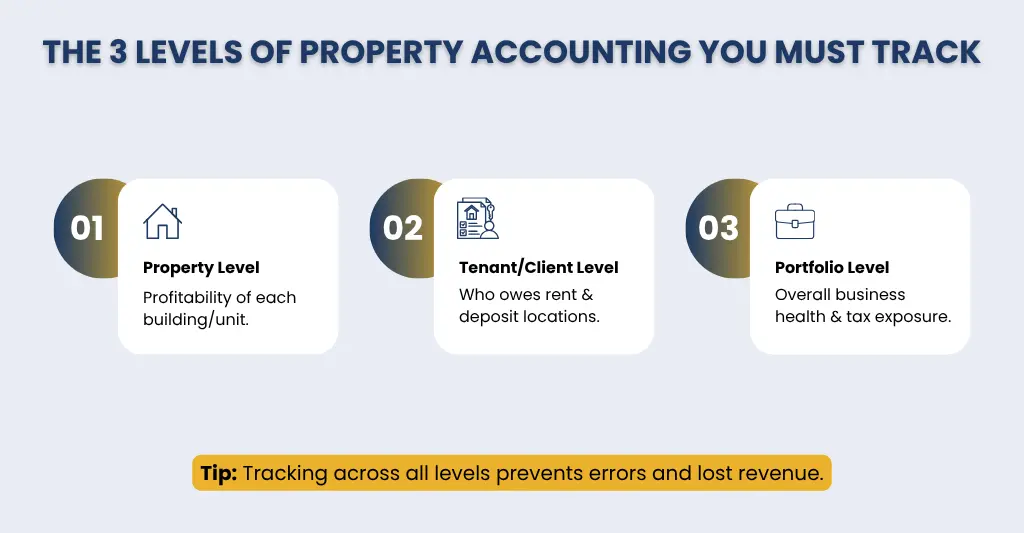

It requires tracking financial health across three distinct layers:

- The Property Level: Is an individual building or unit profitable?

- The Client/Tenant Level: Who owes what, who is in arrears, and whose deposit is held where?

- The Portfolio/Corporate Level: What is the overarching financial health and tax liability of the business or investor?

Common Property Management Accounting Tasks

To maintain an unshakeable financial foundation, property professionals must execute several distinct accounting tasks with absolute precision.

Managing Client Trust Accounts

For estate and letting agents, this is arguably the most critical task. Client trust accounts (often referred to as client money accounts) are distinct bank accounts used exclusively to hold funds belonging to landlords and tenants—such as monthly rental payments, holding fees, and maintenance reserves.

- The Golden Rule: These funds must never be co-mingled with your agency’s operational business accounts.

- Compliance: In the UK, holding client money requires strict adherence to Client Money Protection (CMP) schemes and rigorous, often daily, bank reconciliations to ensure the ledger balance perfectly matches the bank balance.

Rent Collection and Arrears Tracking

This includes creating and sending out rental invoices, capturing rent payments, and spotting late payments as they occur. Real-time and accurate logging helps avoid conflicts and facilitates timely communication on arrears before they become issues, thus avoiding potentially costly litigation.

Tracking Depreciation and Property Value

While property values typically appreciate over the long term, the assets within them degrade. The distinction between capital enhancements (which may offset Capital Gains Tax on the sale of the property) and revenue expenses (day-to-day repairs that may offset income tax) is crucial. Where fixtures, fittings and furnishings have been installed, it is also important for investors to monitor their depreciation to ensure that they are maximising tax relief under capital allowances (if applicable).

Expense Allocation and Invoice Processing

There is no end of costs that come with a property portfolio—gas safety certificates, emergency plumbing, insurance premiums and management fees. Invoices need to be coded and allocated properly into the correct property and owner in order to maintain profitability metrics.

Tax Implications for Property Managers and Landlords

Navigating the UK tax system is one of the most complex aspects of property ownership and management. Failing to account for taxes properly can erode your margins entirely.

How VAT Applies to Property Management Services

Value Added Tax (VAT) in the UK property sector is notoriously complex due to the varying tax statuses of different real estate types:

- Residential Letting: Residential property rentals in the UK are generally VAT-exempt. This means landlords usually cannot charge VAT on rent or reclaim VAT on expenses related to standard residential lettings.

- Property Management Fees: For those property letting or estate agents who provide property management services and have generated more than the current threshold (or opted to register voluntarily), the management fees are subject to the standard rate of VAT (20%) charged to landlords, making accurate VAT reporting and compliance essential.

- Commercial Property: Commercial property transactions may be standard-rated if the owner decides to “opt to tax” the building. This allows VAT to be recovered on repairs, etc., but it also means that VAT will be charged to commercial tenants on rental income.

National Insurance Contributions (NIC) and Other Taxes

The legal structure of your property business dictates how you are taxed:

- Income Tax vs. Corporation Tax: Rental income from properties held in your personal name is subject to Income Tax, which can be as high as 45% depending on your tax band. Under the Section 24 rules, individual landlords cannot fully offset mortgage interest against rental income before tax and instead receive a basic 20% tax credit. As a result, many property investors now operate through a Limited Company (Special Purpose Vehicle), where profits are subject to Corporation Tax and mortgage interest may be fully deductible as a business expense.

- National Insurance Contributions (NIC): If you are a property management business (or are defined as ‘running a property business’ – typically those with a significant number of properties that are actively managed), you may be liable to pay Class 2 or Class 4 National Insurance Contributions on your profits, depending on the structure of your business.

- Stamp Duty Land Tax (SDLT) and Capital Gains Tax (CGT): SDLT is payable (typically 3% plus a surcharge of 1% on additional properties/companies) on the purchase of properties. CGT is payable by the individual when properties are sold (at a higher rate than the tax rates applied to other assets) and Corporation Tax is applied to the gain by companies.

Common Accounting Mistakes and How to Avoid Them

Accounting mistakes can happen at any time, even for seasoned real estate professionals. Early identification of these can be the key to protecting your business.

- Co-mingling Personal and Business Funds: This results in an administrative nightmare because of the co-mingling of Personal and business funds. The Fix: Have separate, dedicated bank accounts for each business entity or for each money stream.

- Misclassifying Repairs vs. Capital Improvements: The distinction between repairs and capital improvements is often a slippery one to make – if a significant structural extension is classified as a repair, rather than a capital improvement, then it will raise instant red flags with HMRC when you file your income tax return. The Fix: Maintain strict definitions. Routine repairs (such as painting, fixing a broken boiler) are revenue expenses. Capital expenditures include such changes or improvements that increase the value of the business, such as a loft conversion.

- Neglecting Receipt and Invoice Management: Not receiving paper receipts means missing out on expenses and profits. The Fix: Use digital scanning solutions to get and maintain a digital copy of the invoice right away.

- Failing to Reconcile Accounts Frequently: Bank reconciliations performed only at the end of the quarter or year can cause errors, fraud, or unallocated tenant deposits to go unnoticed.

Best Practices in Property Management Accounting

Adopting institutional-grade best practices keeps your portfolio agile, transparent, and fully audit-proof.

Shift to the Cloud with Dedicated Software

Relying on manual spreadsheets is a recipe for operational failure. One of the single best practices you can implement is deploying specialised property management accounting software (such as Reapit, Arthur Online, Xero with property integrations, or MRI Software). These platforms automate rent tracking, generate late payment alerts, manage client accounting, track maintenance expenses, and seamlessly integrate with your bank feeds.

Transition to a Double-Entry Accounting System

Because of double entry accounting, each transaction is recorded twice, with two distinct entries (debits and credits). It helps to balance your books with no extra effort on your part, so that investors and auditors can see exactly what’s happening and no money can be lost or go astray.

Build a Robust Cash Reserve

Properties require capital injections for unexpected emergencies (e.g., roof leaks, tenant voids). Best practice dictates setting aside 5% to 10% of monthly gross rental income into a ring-fenced reserve fund per property.

Stay Aligned with Making Tax Digital (MTD)

Making Tax Digital will mandate the use of digital financial records for businesses and individual landlords with an income level above a certain threshold and the submission of quarterly updates online. To prevent future disruptions to your digital accounting system, make sure it is completely MTD compliant. For a detailed breakdown of upcoming requirements and how to prepare, see our guide on MTD for Income Tax: Operational Readiness Guide for UK Businesses (2026).

How E2E UK Property Management Accountants Can Help

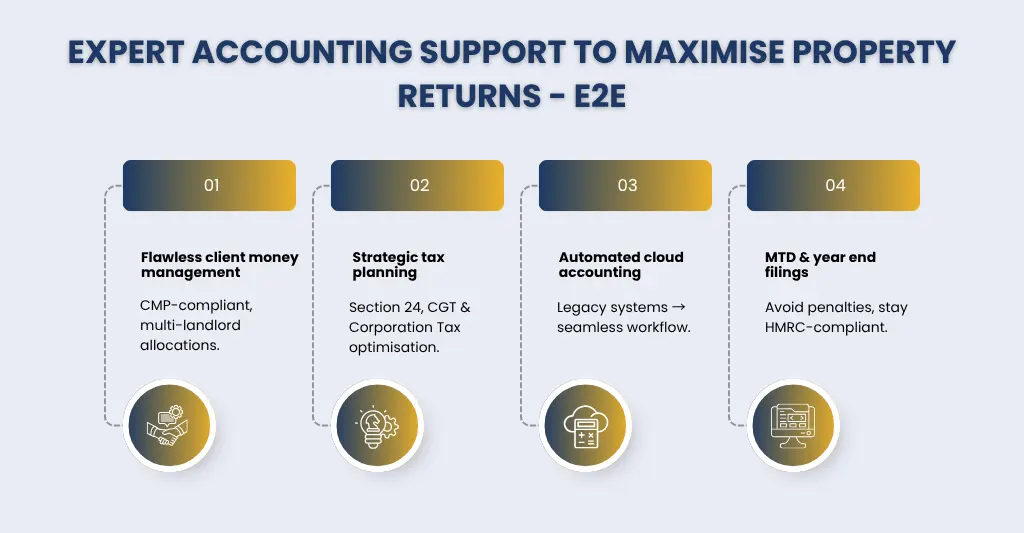

Property accounting is not just time-consuming; it demands highly specialised knowledge of UK property law, HMRC compliance, and financial engineering. This is where partnering with an expert firm like E2E UK Property Management Accountants becomes an invaluable asset.

E2E provides end-to-end accounting infrastructure designed specifically for landlords, investors, and estate agents. Our expert services include:

- Flawless Client Money Management: Ensuring total compliance with CMP regulations and handling complex multi-landlord distributions.

- Strategic Tax Optimisation: Structuring portfolios (e.g. incorporation strategies) to reduce Section 24 impact, Capital Gains Tax and Corporation Tax in a legally compliant way. For deeper insights into practical methods, see our guide on How to Reduce Corporation Tax in the UK: 11 Strategies for 2026.

- Automated Cloud Accounting Setup: Moving legacy systems to the top tier property management accounting software and automating workflows.

- MTD Compliance and Year End Filing: Ensuring all quarterly and annual filings are completed correctly, avoiding HMRC penalties.

Outsourcing your back end to E2E saves you the time, hassle, and stress of managing your finances with spreadsheets while you’re on the hunt for new deals, serving tenants, and expanding your real estate presence.

Conclusion

If you don’t know how to do property management accounting, your property portfolios will barely get by. Without a clear system in place, you risk losing control of funds, missing opportunities for profit, and falling behind on UK tax compliance. Maintaining a clear separation of funds, automating your processes, keeping up with complex UK tax regulations, and avoiding common bookkeeping mistakes helps protect your investments and unlock untapped profits.

Don’t leave your finances until the last minute. Strengthen your accounting practices now—or work with specialist professionals – so you can secure your property portfolio for the future.

People Also Ask:

How to do property management accounting?

Effective property management accounting requires that you have an eye on every dollar you put in and out at each property. First of all, establish dedicated property bank accounts, use double-entry bookkeeping, separate all revenue, expenses and capital expenditure entries, and make use of specific software to automate rent tracking, invoicing, and bank reconciliations.

How do I manage rental income and property expenses for tax compliance?

It is important to have accurate, up-to-date, and digital records of all rental statements and expense receipts to ensure tax compliance. Make sure to keep deductible running costs (such as letting agency charges and safety certificates) apart from capital improvements. Match your property accounts monthly and make sure you use MTD-compliant software so you maintain your records easily and readily available for HMRC submission.

What is a trust account for property management?

A trust account (or client money account) is a specialised bank account used by property managers and estate agents to hold funds belonging to landlords and tenants. This includes rental income, maintenance reserves, and deposits. These accounts are strictly ring-fenced from the agency’s own operational funds to ensure legal safety and compliance.

What is the best property management accounting software for landlords?

The best software depends on portfolio size. Smaller landlords have found cloud-based accounting software (Xero, QuickBooks, etc.) and property software (Hammock, Landlord Studio, etc.) to be a dream come true. Dedicated and advanced systems such as Arthur Online, Reapit, or MRI Software are available for larger estate agents and institutional investors to provide complete tracking and accounting for clients’ portfolios.

How do I avoid common mistakes in property management accounting?

To prevent errors, do not mix personal and business transactions. Reconcile bank transactions regularly (weekly is preferred), don’t leave anything to chance with receipts—scan and log receipts digitally as soon as they are received—and consult a professional property accountant to help you correctly classify more complex capital expenditures versus property repairs.

What are the tax implications of rental income in the UK?

Rental income in the UK will be taxed at the top rate of Income Tax (up to 45%) or Corporation Tax (if held through a Limited Company). Section 24 will introduce mortgage interest relief restrictions for personal landlords, but corporate structures will be able to claim finance costs as a business expense. Property revenue may also impact your VAT obligations and National Insurance liabilities, depending on your business model.