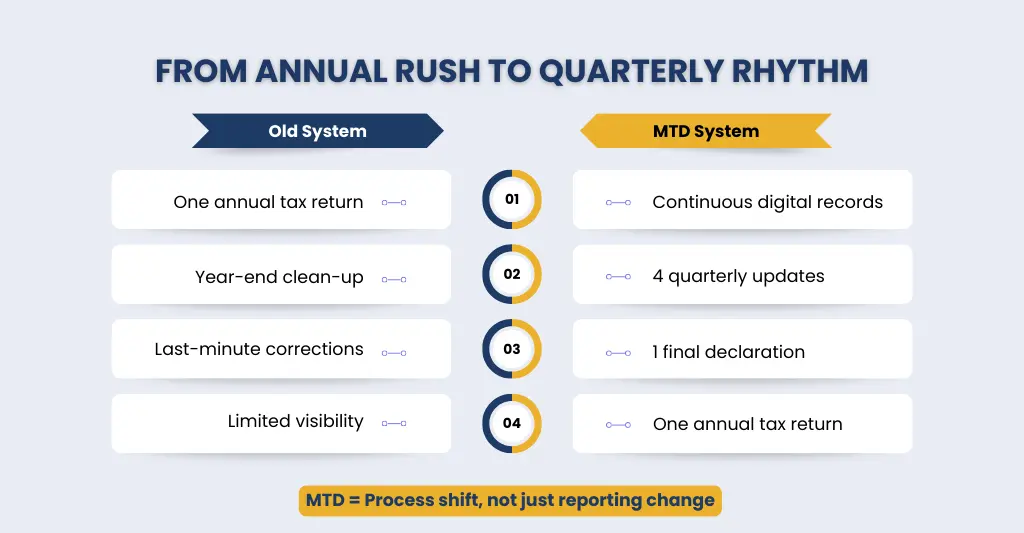

Making Tax Digital for Income Tax represents HMRC’s next major step towards real-time tax reporting. It marks a significant shift in how income is recorded, examined, and reported throughout the year.

The days of annual tax returns and the hassle of last-minute preparation are history. Under MTD for Income Tax, quarterly digital submissions, suitable software, and continuing record-keeping become the new normal.

And for many organisations, the true problem is being operationally ready rather than knowing the regulations.

This blog is meant to help you transition from awareness to action. We explain what MTD for Income Tax means in practice, and who it will affect in 2026. Most importantly, how UK businesses can prepare their systems, processes, and teams to remain compliant without affecting day-to-day operations.

MTD for Income Tax in Practice – What Changes for Businesses

So, what exactly happens when MTD for Income Tax goes into effect? The most significant shift is in frequency. Businesses will no longer wait until the end of the year to bring everything together. Instead, revenue and expenses must be digitally documented and submitted with HMRC every quarter via approved software. Many landlords and self-employed individuals will be required to keep digital records of their business and rental property revenue and expenses under MTD.

These records will be used to create quarterly updates, which must be provided digitally to HMRC.

Who Must Comply From April 2026?

The first phase of Making Tax Digital for Income Tax will become necessary for many UK sole traders and landlords on April 6, 2026. Under this rollout, HMRC will use your total qualifying income, not profit, to determine if you must begin filing your taxes digitally and more frequently.

You must comply from April 2026 if:

- You are a sole trader or landlord enrolled for self assessment.

- Your qualified income from self-employment and/or property exceeds £50,000 for the 2024-25 tax year.

Note: Your qualified income includes gross revenue (before expenses) from self-employment and rental property, not net profit after costs.

HMRC calculates each landlord’s share of gross rental income if the property is jointly owned. For example, if a property earns £60,000 per year and you own 50% of it, just your £30,000 portion counts towards your MTD qualifying income, which is then combined with any other self-employment income you have.

MTD for Income Tax isn’t stopping here. The system is being phased, based on income levels:

- From 6 April 2026: gross qualifying income, over £50,000

- From 6 April 2027: gross qualifying income, over £30,000

- From 6 April 2028: gross qualifying income, over £20,000

These criteria suggest that even if you do not have to comply in 2026, you will have to in the coming years when your income falls into the next band. Because HMRC calculates your start date on the most recent Self Assessment or qualifying income numbers, reviewing your income now ensures you are not caught off guard near the deadline. Early review assists with software selection, reporting habits, and support, lowering stress and assuring compliance before MTD for Income Tax becomes necessary.

If you’re new to Self Assessment, registering for online tax returns early helps avoid delays when MTD for Income Tax becomes mandatory.

Understanding Qualifying Income -The £50,000 Test

According to MTD for Income Tax, the £50,000 test determines who must join the new digital reporting system first.

Qualifying income means your total gross income from:

- Self-employment (before expenses)

- UK or overseas property (before allowable costs)

If the total of these exceeds £50,000 in a tax year, you will be required to use MTD for Income Tax beginning April 2026, according to figures reported by HM Revenue & Customs (HMRC).

Key points to know:

- It is gross income, not profit (expenses do not lower the sum).

- PAYE income (such as salary or pensions) does not contribute towards the £50,000 test.

- This evaluation is based on your most recent tax return.

- If you’re under £50,000, MTD may still apply later if thresholds are reduced.

These criteria suggest that even if you do not have to comply in 2026, you may be required to do so the following year if your income falls into the next band.

Sector-Specific Impact of MTD for Income Tax

MTD for Income Tax does not affect all businesses/sectors in the same way. The reporting burden, data complexity, and compliance risk differ significantly with transaction volume, income streams, and cost patterns – driving the majority of the variation.

eCommerce & Online Sellers:

The most difficult aspect of quarterly reporting is the high volume of transactions. Sales pass through marketplaces, payment gateways, refunds, chargebacks, and fees, often resulting in net payouts rather than clear invoices.

MTD requires vendors to keep digitally linked records and submit quarterly updates, which means:

- Marketplace fees and VAT must be tracked accurately

- Reconciliations can no longer wait until year end

- Poor integrations between platforms and accounting software increase error risk

Property & Landlords:

MTD speeds up compliance for landlords. Rental revenue and allowed expenses must be recorded and reported quarterly rather than once a year.

Key impacts include:

- Gross rental income is used for MTD thresholds, not profit

- Multiple properties increase reporting complexity. Hence, specialist property accountants become crucial.

- Inconsistent record-keeping (spreadsheets, paper receipts) becomes non-compliant.

Construction & Trades:

Trades and construction enterprises frequently deal with unpredictable income, subcontractors, and CIS deductions. MTD increases the demand for real-time accuracy.

Common pressure points:

- Quarterly reporting alongside CIS obligations

- Tracking materials, labour, and job-based costs digitally

- Reduced margin for correcting errors at year-end

Solicitors, Conveyancers & Professional Services:

Professional firms deal with fee income, retainers, disbursements, and client accounts, which may not necessarily fit neatly into traditional bookkeeping.

MTD impact includes:

- More frequent reporting of gross income

- Greater scrutiny of expense categorisation

- Stronger reliance on compliant accounting software and processes

Dental, Hospitality & Recruitment:

These industries face volume-driven complexity rather than straightforward income reporting.

- Dental and hospitality firms manage daily sales, card settlements, tips, and staffing expenditures.

- Recruitment firms deal with contractor payroll, bills, and cash flow timing concerns.

Quarterly filings to HM Revenue & Customs under MTD mean fewer opportunities to “fix it later”, making clean, consistent bookkeeping vital across all of these sectors.

MTD for Income Tax Self Assessment – Reporting & Deadlines

Making Tax Digital (MTD) for Income Tax Self Assessment alters the frequency and manner in which self-employed individuals and landlords report income to HM Revenue & Customs. The annual tax return does not disappear, but it is no longer the main event.

Quarterly Updates (Ongoing Reporting):

Instead of making one annual submission, you’ll provide four quarterly updates via MTD-compatible software. These are summarised reports, not complete tax calculations.

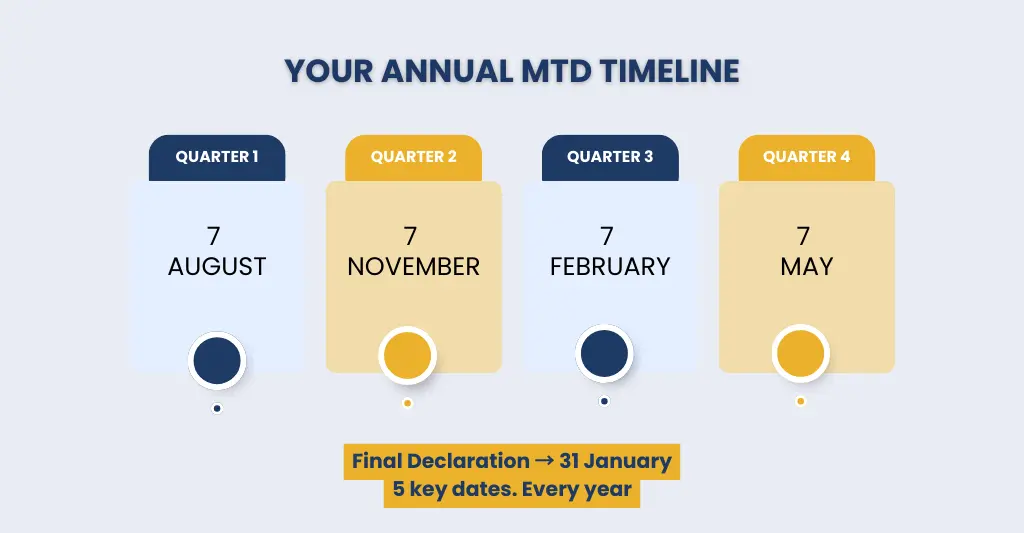

Typical quarterly periods:

- Quarter 1 (6 Apr- 5 Jul): 7 August

- Quarter 2 (6 Jul – 5 Oct): 7 November

- Quarter 3 (6 Oct – 5 Jan): 7 February

- Quarter 4 (6 Jan – 5 Apr): 7 May

Each update includes:

- Total income for the period (self-employment and/or property)

- Allowable expenses

- Digitally linked records (no manual re-keying)

End of Period Statement (EOPS)

After the tax year ends, you must submit an End of Period Statement for each income source. This finalises:

- Adjustments and accounting corrections

- Capital allowances

- Reliefs not included in quarterly updates

Deadline: 31 January following the tax year.

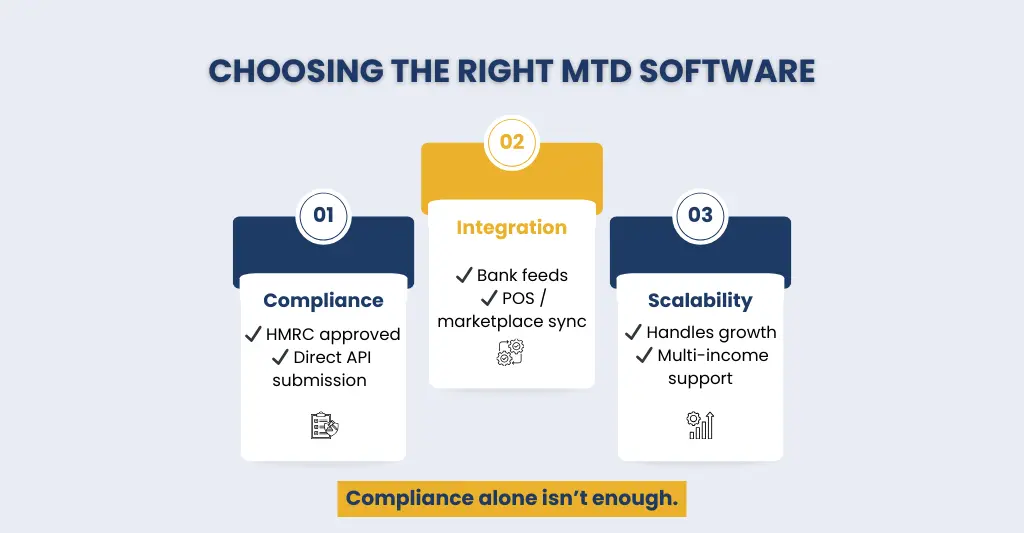

MTD-Compatible Software – What You Need

To meet the Making Tax Digital (MTD) for Income Tax requirements, you must use HMRC-approved MTD-compatible software. You can select between entire full accounting and record-keeping platforms or bridging and specialist tools to connect your data to HMRC’s system.

Here are some commonly used MTD-compatible software options:

Full Accounting & Record-Keeping Platforms:

These platforms support digital bookkeeping, bank feeds, expense monitoring, and direct HMRC submissions, making them perfect for sole traders, landlords, and small firms.

- Sage Accounting / Sage Business Cloud – Cloud accounting with bookkeeping, invoicing, expenses, and MTD submissions.

- QuickBooks Online – Popular cloud accounting software with full MTD compliance and easy HMRC connection.

- Xero – Cloud-based tool offering digital records, bank reconciliation, and HMRC linking for tax submissions.

- FreeAgent – UK-focused accounting platform suited for sole traders and freelancers with direct MTD support.

- Zoho Books – Cloud accounting with digital record keeping and HMRC MTD integration.

- Clear Books – HMRC-recognised bookkeeping tool with free versions for basic users.

- QuickFile Accounting – A user-friendly cloud option supporting MTD submissions.

Bridging & Specialist Tools:

If you choose to continue using spreadsheets or existing systems, bridging software connects your data to HMRC’s API to ensure compliant filings.

- 123 Sheets (bridging for spreadsheets) – Converts Excel/Sheets into MTD-compliant submissions.

- TaxCalc / Capium / IRIS Kashflow – Established accounting packages with bridging or full MTD support.

- Hammock (for landlords) and RentalBux – Tools focused on property income and MTD compliance.

Preparing Your Business – Operational Checklist

Getting ready for MTD for Income Tax is more than just software; it’s also about tightening the day-to-day financial operations that fuel your reports. Use this checklist to ensure that your firm is MTD-ready rather than MTD-stressed.

- Confirm Your MTD Status:

- Check if your qualified income exceeds the MTD threshold.

- Identify all revenue sources (self-employment, property, and numerous trades).

- Confirm when you will be mandated into the MTD.

- Choose MTD-Compatible Software:

- Choose software that enables digital record-keeping and quarterly submissions.

- Make sure it works with your bank feeds, invoicing, and expense tools.

- Avoid manual data transfers that violate digital linking requirements.

- Set Quarterly Reporting Routines:

- Schedule internal deadlines ahead of HMRC’s submission dates.

- Schedule monthly reconciliations to prevent last-minute fixes.

- Assign responsibility for review and submission.

- Align With Your Accountant or Outsourcing Partner:

- Determine who handles bookkeeping, reviews, and submissions.

- Agree on dates, data transfers, and responsibilities.

- Integrate MTD compliance into your ongoing financial strategy.

Bonus – You can use customised management accounts to forecast cash flow, get a real-time snapshot of your financial performance, and take strategic decisions early and efficiently.

Unsure if you’re ready for MTD for Income Tax? Download our free 2026 MTD checklist and score your readiness in minutes

Common MTD Risks That Lead to Penalties

MTD for Income Tax reduces the margin of error. Penalties are based on process failings rather than intent. Here are the most prevalent risks that businesses face, and how they occur.

- Missing Quarterly Deadlines: Quarterly reports are required. Late submissions, even if no tax is payable, may result in fines under HM Revenue & Customs’ new points-based system.

- Why does it happen?

- Treating updates like “drafts” instead of formal submissions

- Leaving reporting until the last few days

- No internal reminders or reporting speed.

- Why does it happen?

- Using Non-Compliant Software: Spreadsheets alone (without bridging software) or manual rekeying across systems violates MTD standards.

- Why does it happen?

- Relying on outdated bookkeeping practices

- Assuming Excel remains acceptable on its own.

- Lack of digital connections between systems

- Why does it happen?

- Leaving Adjustments Until Year End: MTD expects cleaner statistics throughout the year. Continuous corrections at the end trigger red flags.

- Why does it happen?

- Treating quarterly updates casually

- Relying on accountants to “fix it later”

- No review before submission

- Why does it happen?

- Manual Data Re-Entry Between Systems: Manual copy-paste disrupts digital links and raises error risk, undermining MTD compliance.

- Why does it happen?

- Bank, POS, and accounting software are not integrated

- Exporting reports instead of syncing data

- Lack of automation in bookkeeping workflows

- Why does it happen?

- Incorrect or Late MTD Registration: If you submit changes before completing formal registration, HMRC may not recognise your filings.

- Why does it happen?

- Registering too close to the initial filing date

- Misunderstanding which income streams qualify.

- Assuming agents have enrolled on your behalf

- Why does it happen?

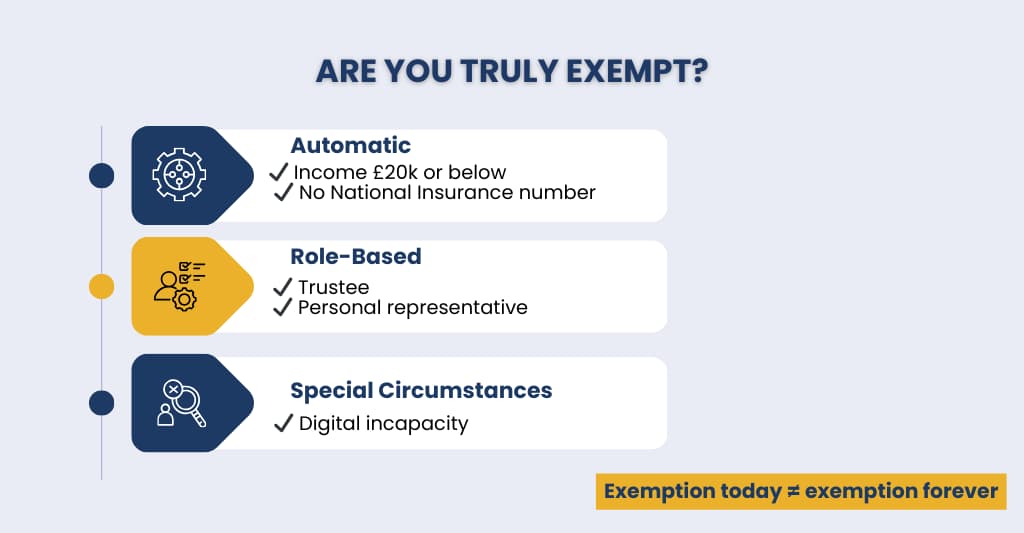

Exemptions & Edge Cases Businesses Often Miss

MTD regulations are not always black and white. Many firms believe they are either totally in or fully out; however, HMRC has various exemptions and edge cases that are frequently misinterpreted or overlooked altogether.

Types of Exemptions:

- Some people are excluded from Making Tax Digital for Income Tax due to their income level, personal circumstances, or the role they play in filing a tax return.

- Exemptions might be permanent (applicable until your circumstances change) or temporary (usually valid until April 2027 at the latest).

Automatic Exemptions (No Application Required):

- If your qualifying income is £20,000 or less, you are automatically exempt from MTD for Income Tax, and you do not need to sign up unless your income exceeds this amount.

- You are automatically exempt if you do not have a National Insurance number because you cannot register for MTD without one.

Exemptions Based on Your Role:

- You are automatically exempt if you file a tax return on behalf of a non-resident firm. Automatic exemption can happen if you serve as a trustee, including charitable trustees and trustees of non-registered pension schemes.

- You are automatically exempted if you are the personal representative of someone who has died.

- If you earn money from self-employment or property ownership outside of these roles, you may still be required to use MTD.

Other Automatic Exemptions:

- If you are a Lloyd’s member and submit a tax return for underwriting business, you are automatically exempt.

- You are automatically exempt if you are physically or mentally incapable of using digital systems and have either obtained a lasting or permanent power of attorney or have a court-appointed deputy managing your affairs.

Why Are Businesses Moving to Sector-Specialist MTD Accountants?

MTD is more than just a compliance modification; it is a transformation in operations. As quarterly reporting becomes the standard, many organisations realise that generalist accounting support isn’t always sufficient, especially if their industry has complex income flows or reporting rules.

- Industry-specific income structures: eCommerce sellers, landlords, contractors, and professional services all create different types of income. MTD accountants who specialise in a specific industry understand these subtleties and treat clients correctly from the start.

- Fewer errors in quarterly submissions: Specialists understand what “normal” looks like in a certain area, making it easier to identify irregularities before submissions raise HMRC red flags.

- Reduced reliance on year-end clean-ups: Sector-specific methods keep records cleaner all year, reducing last-minute revisions and compliance risk.

- Better handling of allowable expenses: What constitutes an authorised cost varies according to industry. Specialists help to ensure that nothing is overlooked or mistakenly claimed.

- MTD-ready software tailored to the sector: Specialists use technologies developed for certain business models, such as property management systems, point of sale, and marketplace integrations.

- Clearer forecasting and cash-flow visibility: Quarterly data is more useful when organised around sector standards and seasonal patterns.

Why Choose E2E Accounting UK for MTD for Income Tax?

E2E Accounting UK helps businesses confidently navigate the entire MTD for Income Tax journey by combining UK tax experience with organised, quarter-by-quarter compliance.

Rather than viewing MTD as a once-a-year requirement, we assist businesses in integrating accurate digital record-keeping and timely reporting into their day-to-day operations, lowering the risk of penalties and last-minute corrections.

Our staff specialises in UK tax and MTD rules, ensuring that your quarterly updates, final declarations, and digital records meet HMRC’s exacting standards. We use HMRC-approved, MTD-compatible software to create clean digital links while removing the hazards associated with manual data processing or outdated systems.

E2E Accounting UK provides comprehensive services, including bookkeeping, reconciliations, quarterly reports, and continuing reviews. This means your stats are verified and refined throughout the year, rather than “fixed at the end,” yielding more dependable data and fewer HMRC red flags. We also detect abnormalities or discrepancies early on, allowing issues to be remedied before submission deadlines.

People Also Ask:

When does MTD for Income Tax start?

MTD for income tax begins on April 6, 2026, for self-employed individuals and landlords earning more than £50,000. Those earning between £30,000 and £50,000 will be eligible to join beginning in April 2027.

How do I calculate my gross income for MTD thresholds?

Total your business and property income before expenses for the tax year. This comprises sales, fees, rent, and other trading income, without deducting expenses. If you have more than one income source, combine them to see if you exceed the MTD level.

Do landlords and sole traders follow the same MTD rules?

Mostly, yes. Landlords and sole traders both use MTD for income tax, which requires them to keep digital records and submit quarterly updates using approved software. The major distinction is how income is reported: rental income for landlords versus trading income for sole traders. If you have both, your income is added together to determine if you meet the MTD level.

Do I need to register separately for MTD?

Yes. The MTD for Income Tax does not apply automatically. If you are in scope, you must register for MTD with HMRC before your first quarterly submission, even if you already file a Self Assessment.

What happens if I miss a quarterly update?

HMRC’s MTD points system may result in you receiving a penalty point. Every time you miss a deadline, you get points, and if you hit the maximum, you face financial penalties. Missing updates can also raise the likelihood of HMRC inspections.

What is MTD for ITSA, and does it apply to me?

MTD for ITSA (Making Tax Digital for Income Tax Self Assessment) is HMRC’s system that mandates digital record-keeping and quarterly income updates rather than a single annual return. It applies to self-employed workers and landlords whose combined gross income exceeds the MTD threshold. If you earn less than the threshold, it does not apply right now, but you should keep an eye on it as the rules are gradually implemented.

How can E2E Accounting UK help me stay MTD compliant?

E2E Accounting UK keeps you MTD compliant by handling digital record-keeping, quarterly updates, and HMRC submissions for you. We utilise MTD-approved software, examine your data before each submission, identify concerns early, and ensure deadlines are never missed, so you can stay compliant without the burden of handling it yourself.