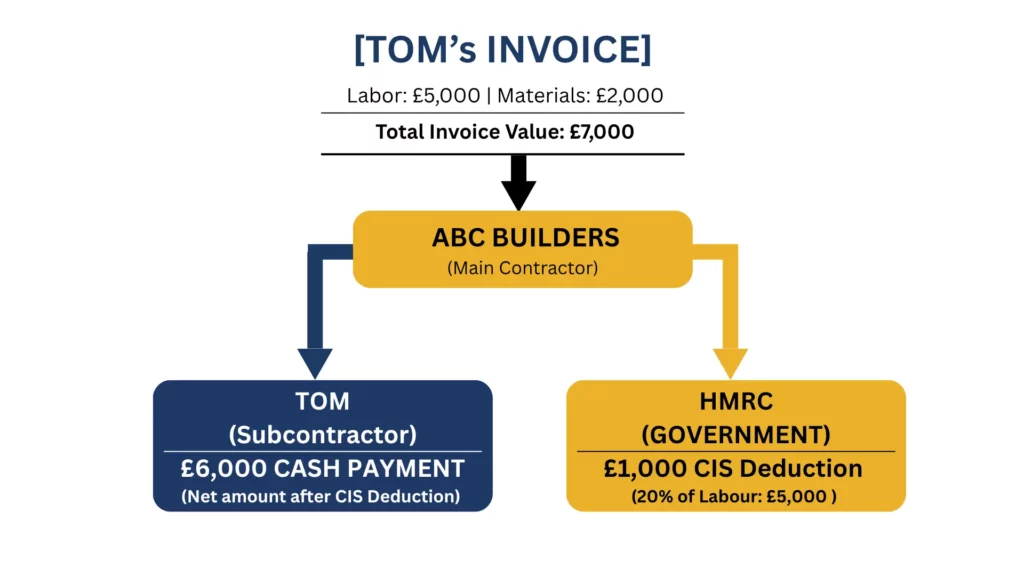

Meet Tom. Tom runs a successful bricklaying business as a subcontractor. He just finished a major phase of a commercial build for a main contractor, ABC Builders. Tom sits down to write his invoice. He knows he’s charging £5,000 for his team’s labour and £2,000 for the bricks they used.

In the past, he would have just added 20% VAT to the whole thing, sent it off, and waited for his money. But today, ABC Builders is registered for both schemes, which are CIS and VAT, and so is Tom. Suddenly, Tom’s £7,000 job turns into a complex math puzzle. He has to deduct tax on only a portion of the bill, mention a tax rate he isn’t actually collecting, and figure out exactly how much cash will land in his bank account so he can pay his lads on Friday.

Calculating tax on the same bill can be incredibly complex. Successfully managing CIS and VAT for construction firms is no longer just an exercise in avoiding HMRC penalties; it is essential to keep your business liquid and maintain your professional reputation. This guide offers an in-depth look at how these requirements intersect and how to handle them simultaneously.

Understanding CIS for Construction Subcontractors

The Construction Industry Scheme (CIS) is a specific system of tax rules for people working in the construction industry. It was designed to keep subcontractors within the tax system, as they frequently move from one project to another.

CIS enables a main contractor to withhold money from a subcontractor’s payment and pass it straight to HMRC. These deductions count as advance payments toward the subcontractor’s ultimate tax and National Insurance bill.

Secondary Guide: How do I register for CIS?

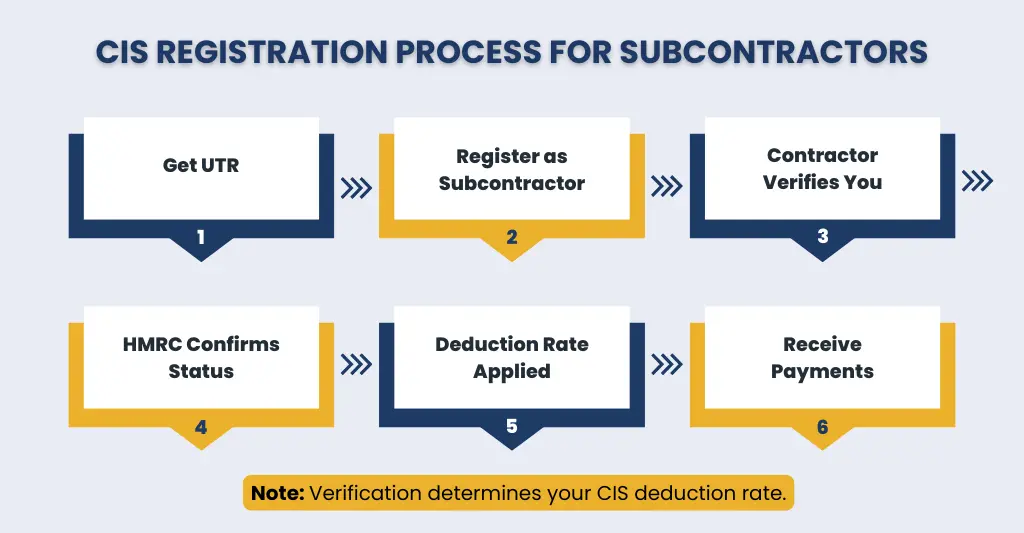

If you operate as a subcontractor, you must register for the scheme whether you are a sole trader, a partner in a firm, or a director of a limited company. If you are wondering, “How do I register for CIS?” the process follows these primary steps:

- Obtain a UTR: You cannot register without a Unique Taxpayer Reference.

- Register as a Subcontractor: You can do this via the HMRC website using your National Insurance number and business UTR.

- The Verification Process: Before a contractor can pay a subcontractor for the first time, they must verify them with the HMRC. This determines the deduction rate. If a contractor fails to verify and applies the wrong rate, they are personally liable for the shortfall.

CIS Deduction Rules and Rates

HMRC sets the deduction rates based on the subcontractor’s registration status:

- 30% (Unregistered): Applied if HMRC cannot verify the subcontractor.

- 20% (Registered): The standard rate for verified subcontractors.

- 0% (Gross Payment Status): For firms with a perfect compliance history and high turnover.

What is a “deductible”?

A common mistake is applying CIS to the entire invoice amount. CIS is only deducted from the labor element. You must exclude VAT; the cost of materials, equipment hired without an operator, and fuel used for plant machinery.

The Intersection of CIS and VAT

The financial picture gets complicated when CIS and the VAT reverse charge (specifically the Domestic Reverse Charge, or DRC) apply to the same invoice. Balancing both requires a deep understanding of how regulations affect CIS and VAT for construction firms. Let’s look at how Tom’s invoice to ABC Builders actually works in practice.

When both schemes apply, Tom does not charge ABC Builders the £1,400 of VAT. Instead, the VAT reverse charge rules dictate that ABC Builders notes the VAT but pays it directly to HMRC on their own return. Simultaneously, ABC Builders must deduct 20% from Tom’s £5,000 labor costs (£1,000) and send that to HMRC too.

In the end, Tom receives £6,000 in cash. Mastering this workflow is critical when setting up robust bookkeeping for CIS and VAT for construction firms.

When Does the Reverse Charge Apply?

The VAT reverse charge applies to most B2B construction services reported under CIS. However, it does not apply if:

- The services are zero-rated (e.g., building new residential housing).

- The customer is an “End User” (e.g., a retail store owner changing their own shop lot).

- The supplier and customer are connected within the same corporate group.

Invoicing CIS and VAT Correctly

For business owners, formatting the physical invoice is often the biggest hurdle. To keep administrative systems compliant with rules governing CIS and VAT for construction firms, you must ensure the VAT reverse charge is displayed transparently. You do not add the VAT amount to the final balance due, but you must clearly state the VAT rate, the reverse charge amount, and a specific legal note.

Sample Invoice Structure

| Item | Calculation | Amount |

| Labor | 5 days of bricklaying | £5,000 |

| Materials | Bricks and mortar | £2,000 |

| Subtotal (Net) | – | £7,000 |

| VAT (20% Reverse Charge) | £7,000 x 20% (Not added to total) | £1,400 (Note: “Domestic Reverse Charge applies. Customer to account for VAT to HMRC.”) |

| CIS Deduction | 20% of £5,000 Labor only | -£1,000 |

| Total Cash Payable to Subcontractor | (£7,000 Net – £1,000 CIS) | £6,000 |

If you forget to include the explicit reverse charge wording on your invoice, HMRC can hold you liable to pay that VAT yourself—even if you never collected it! This is why automating CIS and VAT for construction firms through specialised platforms is highly recommended.

Managing Dual Registration

Can a construction firm be both CIS and VAT registered?

Yes, and most scaling businesses are. Successfully balancing dual enrollment is a standard milestone when managing CIS and VAT for construction firms. For expert guidance, see our dedicated blog on bookkeeping for the construction industry.

- VAT Registration: Mandatory if your taxable turnover exceeds £90,000.

- CIS Registration: Mandatory for anyone working as a subcontractor for other contractors.

Because of the VAT reverse charge, many subcontractors find themselves in a permanent “VAT refund” position. They pay VAT on materials they buy (Input VAT) but do not collect VAT on their invoices. This leaves them constantly owing money to HMRC. Efficiently tracking CIS and VAT for construction firms ensures these VAT refunds are claimed promptly to protect your cash flow.

Software Solutions for Construction Firms

Trying to track these calculations manually using spreadsheets is a recipe for expensive errors. Modern companies rely on dedicated cloud and construction accounting software to simplify CIS and VAT for construction firms:

- Direct HMRC Verification: Automatically checks subcontractor UTRs and tax statuses, solving the common question of how do I register for CIS and verify others.

- Automated Reverse Charge Rules: Recognises when both parties are registered and applies the correct VAT reverse charge invoice wording and tax mapping automatically.

- Instant CIS Statements: Generates and emails monthly payment statements straight to your subcontractors.

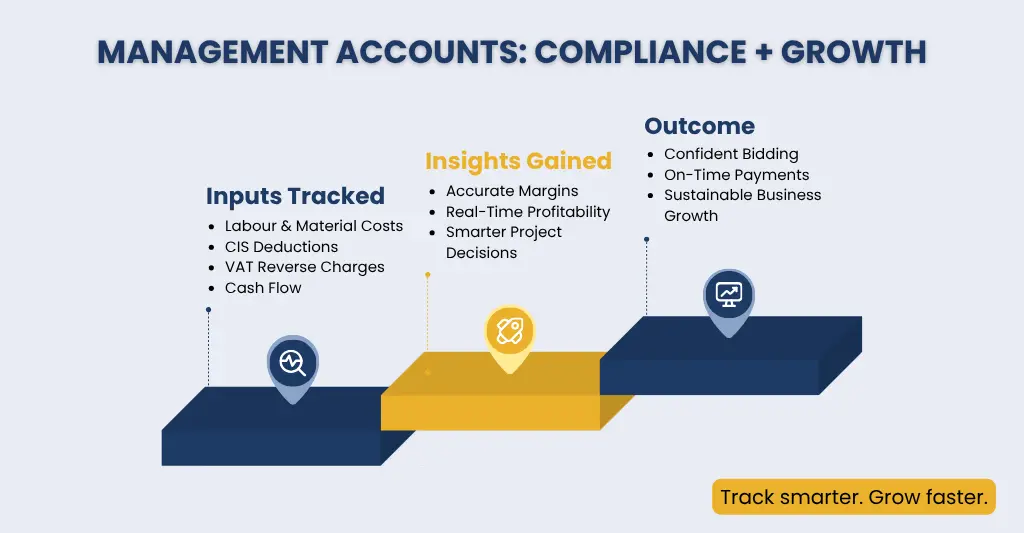

Conclusion: Driving Growth with Management Accounts

Staying compliant with CIS and VAT for construction firms keeps HMRC happy, but compliance alone won’t grow your business. This is where management accounts become your secret weapon.

Traditional compliance accounting looks backwards—telling you what you owed last quarter. Management accounts look forward. Because the intersection of CIS deductions and the VAT reverse charge directly impacts your day-to-day cash reserves, having quarterly or monthly management reports gives you real-time clarity.

By analysing your gross margins, tracking your exact CIS refund positions, and forecasting cash flow fluctuations before they happen, management accounts empower construction firms and subcontractors alike to make informed decisions. You can confidently bid on larger contracts, purchase materials in bulk, and scale your operations sustainably without running out of working capital.

Why Choose E2E Accounting for Construction Compliance

At E2E Accounting, we specialise in taking the complexity out of compliance. We help businesses build robust invoicing frameworks tailored explicitly to handle CIS and VAT for construction firms alongside Work-in-Progress (WIP) accounting seamlessly.

Whether you are a sole trader trying to figure out your next invoice or a large firm struggling with monthly reconciliations, our expert guidance ensures you stay compliant while you focus on the build. Contact E2E Accounting today for a simplified approach to construction tax.

People Also Ask:

How do I register for CIS as a construction subcontractor?

If you are asking how do I register for CIS, you can quickly complete the process via the HMRC online service using your UTR and National Insurance number. If you operate as a limited company, you must register the company itself rather than yourself as an individual.

Can a construction firm be CIS registered and VAT registered at the same time?

Absolutely. Most growing businesses are. You must be CIS registered to work for other contractors, and VAT registration is mandatory once your taxable turnover hits £90,000. Managing CIS and VAT for construction firms simultaneously is a clear sign of a scaling, legitimate enterprise.

Does the VAT reverse charge apply to materials?

Yes, if they are supplied as part of a service that includes labour (a “supply and fix” contract). If you are providing both the labor and the materials, the entire invoice value falls under the reverse charge rules. If you are only selling materials to a site without installation, standard VAT rules apply.

How should a construction company invoice VAT and CIS correctly?

Invoices should show the net labour and materials, the CIS deduction (on labour only), and—if the reverse charge applies—the VAT amount with a note that the customer is responsible for paying it to HMRC.

What is the VAT reverse charge, and how does it apply to construction services?

It is a rule where the customer accounts for VAT instead of the supplier. It applies to services reported under CIS between two VAT-registered businesses.

What deductions do I need to make for CIS?

Standard registered subcontractors have 20% deducted. Unregistered ones have 30% deducted. Gross Payment Status: Subcontractors have 0% deducted.

Are all construction subcontractors affected by CIS?

Yes, except for those that only offer professional services such as architecture, surveying, or building consultancy.

Can CIS accounting software help automate compliance?

Absolutely. It automates verification, deduction calculations, and the generation of mandatory payment statements.

How do I claim a CIS tax refund?

Because of how deductions work, subcontractors often overpay taxes throughout the year. Sole traders claim this back through their annual Self Assessment. Limited companies can offset their CIS credits monthly against their PAYE/National Insurance liabilities or claim a refund directly from HMRC at the end of the tax year.

Does the Reverse Charge apply if my customer is not VAT registered?

No. The Domestic Reverse Charge is only triggered if both the supplier and the customer are registered for VAT and the transaction falls under CIS. If your customer is a private homeowner or a non-VAT registered business, you apply standard VAT rules rather than the VAT reverse charge.

What are the penalties for incorrect CIS or VAT filings in construction?

Late CIS returns result in an immediate £100 penalty, which escalates over time. Incorrect VAT reporting or missing documentation under the VAT reverse charge framework can lead to severe interest charges, percentage-based surcharges, and direct HMRC audits.