Online sales seems easier from the outside: you list a product, buyers purchase it, and money is received quickly. In reality, the behind-the-scenes scenario is totally different.

Daily sales across platforms, payment gateways, shipping expenses, frequent returns, marketplace commissions, and inventory changes are all challenges faced by online merchants. If improperly tracked, it can result in accounting confusion. Inaccurate VAT returns, bad cash flow decisions, or profit margins that appear robust but are not, can result from a few missed numbers.

The most crucial accounting practices for online retailers will be covered in this blog so you can maintain compliance, safeguard your earnings, and create a retail company that expands without financial strain.

What Makes Accounting for Online Retailers Different?

When sales, expenses, and payments don’t all occur in a single cycle, accounting for online shops is more complicated than for traditional organisations.

The amount you “sell” is frequently different from the amount you actually receive in the bank because online shops deal with several selling platforms (Amazon, Shopify, eBay, WooCommerce), payment processors (Stripe, PayPal), and marketplace deductions, unlike traditional stores.

Here’s what makes eCommerce accounting different:

- High-volume transactions: Hundreds (or thousands) of small orders make bookkeeping more detailed.

- Marketplace fees & commissions: Amazon and other platforms deduct referral fees, FBA charges, storage fees, etc.

- Refunds, returns & chargebacks: These affect revenue and profit, and must be recorded correctly.

- Inventory tracking: Stock levels change daily, and inventory is directly linked to profit calculation.

- Shipping & fulfilment costs: Costs vary by order, location, and logistics partner, impacting margins.

- VAT and cross-border sales: Online retailers often sell across regions, making VAT compliance tricky.

- Cash flow gaps: You may sell today but receive payments after several days or weeks, especially on marketplaces.

Core Accounting Practices Every Online Retailer Should Follow

Online shops require robust accounting systems from the start to maintain profitability and prevent cash-flow or tax shocks. Due to the large rate of sales, various fees, refunds, inventory movement, and platform payouts associated with eCommerce, little mistakes can easily escalate into significant financial confusion.

The following are the most crucial accounting procedures that any online retailer should adhere to:

- Real-Time Bookkeeping: Keep accurate records of all sales, expenses, refunds, and fees. Bookkeeping should be updated on a weekly or even daily basis, rather than only once a month, since online firms produce everyday transactions.

- Reconcile Bank, Payment Gateways, and Marketplaces: Your bank statement alone is not enough. Always reconcile:

- Bank transactions

- Stripe/PayPal settlements

- Amazon/Shopify payouts

This ensures your revenue and fees are recorded correctly.

- Track Marketplace Fees Separately: Platforms deduct multiple charges (commission, fulfilment, storage, subscription fees). If you don’t track them separately, your profits will look higher than they really are.

- Monitor Inventory Properly: Inventory is one of the biggest reasons eCommerce accounting goes wrong. Track:

- Opening stock

- Purchases

- Closing stock

- Dead/slow-moving inventory

This is essential for accurate cost of goods sold (COGS) and profit margins.

- Use Consistent Accounting Categories: Standardise your chart of accounts (COA) so your reporting stays accurate. For example:

- Ad spend

- Shipping/fulfilment

- Platform fees

- Subscriptions

- Returns/refunds

Common Accounting Mistakes Online Retailers Make

At first glance, online retail accounting may appear straightforward: funds are received, orders are placed, and costs are covered. However, mistakes are frequently made in eCommerce finance due to the numerous platforms, fees, refunds, and inventory transfers involved (particularly during expansion).

The most common accounting errors made by internet businesses are as follows:

- Treating Sales as Profit: A lot of retailers believe that strong sales equate to high profits. However, the earnings picture might change significantly after deducting platform fees, fulfilment expenses, returns, taxes, and ad expenditure.

- Ignoring Inventory Accounting: Inventory mistakes are one of the biggest reasons financial reports become unreliable. Common issues include:

- not updating stock values

- not tracking dead stock

- inaccurate COGS

Without proper inventory tracking, profit margins become guesswork.

- Not Tracking Returns and Refunds Correctly: Refunds are often handled as “missing income” or improperly recorded by shops. This results in erroneous monthly reporting and VAT computations.

- Waiting Until Year End to Fix Accounts: Online retailers often delay bookkeeping until tax season. Later, what happens:

- errors pile up

- Reconciliations become harder

- Financial decisions are based on incomplete data

- Mixing Business and Personal Transactions: Mixing business expenses & transactions with personal accounts is still faced by even the large companies. This, in turn, decreases cash flow visibility, complicates bookkeeping, and may cause problems with tax filing compliance.

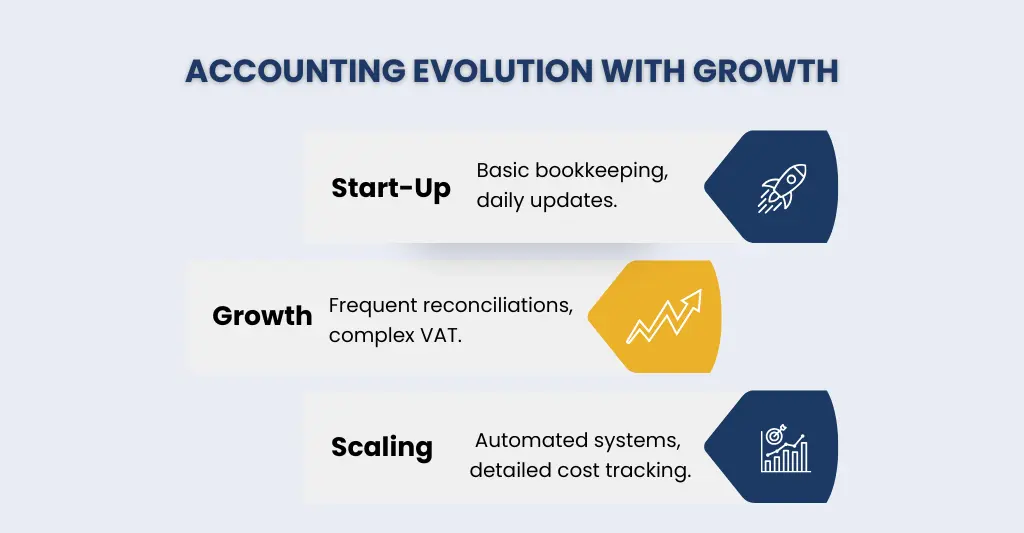

How Accounting Practices Change as Online Retailers Grow

Earlier, basic bookkeeping, tracking sales, expenses, and bank payments, was generally sufficient for online shops to manage their finances. However, as your store expands, accounting becomes more about profit management, cash flow planning, compliance, and strategic decision-making than it is about “record keeping.”

Here is a detailed explanation of how accounting procedures change as online merchants grow, along with the adjustments you need to make at each stage.

- Bookkeeping becomes more frequent: Updates every month are no longer sufficient. To maintain accuracy, growing shops require weekly (or even daily) tracking.

- Reconciliation becomes critical: To prevent revenue errors, bank transactions must be reconciled with Shopify/Amazon payouts, Stripe/PayPal settlements, and platform fee deductions.

- Inventory tracking becomes essential: Accurate inventory value and COGS computation are critical to profit reporting. Margins are unreliable without this.

- Cost tracking gets more detailed: To determine genuine profitability, fees, fulfilment expenses, returns, packaging, and advertising expenditures – all must be appropriately classified.

- VAT and compliance become more complex: Expansion across platforms and regions increases VAT responsibilities and the risk of HMRC mistakes.

- Cash flow becomes forecast-driven: Cash flow planning is necessary for larger advertising expenditures and bulk product purchases, not merely checking bank balances.

- Systems replace spreadsheets: Automation tools and integrations become essential for error-free handling of high-volume transactions.

Tools and Systems Commonly Used by Online Retailers

Relying solely on spreadsheets becomes dangerous as a firm expands because online merchants deal with high-volume transactions, frequent refunds, different payment methods, and inventory movement.

The majority of eCommerce companies require integrated solutions that combine their accounting software, inventories, and reporting solutions to maintain accuracy, scalability, and tax compliance.

Here are the most commonly used tools and systems online retailers rely on:

#1 Cloud Accounting Software (Core System):

This is the main platform where your bookkeeping, bank reconciliation, VAT reporting, and financial statements are managed.

Most used tools:

- Xero (very popular with UK retailers)

- QuickBooks Online

- Sage Accounting (more common in UK SMEs)

#2 eCommerce Platform & Storefront Systems:

These tools manage product listings, checkout, order tracking, and customer payments.

Most used tools:

- Shopify

- WooCommerce

- BigCommerce

- Magento (Adobe Commerce)

#3 Payment Gateways & Merchant Services:

These tools process customer card payments and often deduct transaction charges before paying you.

Most used tools:

- Stripe

- PayPal

- Square

- Klarna / Clearpay (Afterpay)

#4 Reporting & Dashboards (For Decision-Making):

Retailers use dashboards to track performance beyond basic profit/loss.

Most common tools:

- Google Looker Studio

- Power BI

- Fathom / Spotlight Reporting

- Xero Analytics (or built-in reports)

Conclusion

Maintaining total control over cash flow, inventory, platform fees, refunds, and tax compliance are all important aspects of accounting for online shops. Due to the fact that eCommerce companies employ a variety of platforms and payment methods, even small accounting mistakes can have a significant effect on profitability.

Online shops can create accurate financial records, comprehend genuine margins, remain compliant, and grow with confidence by adhering to sound accounting procedures, avoiding typical errors, and utilising the appropriate tools and methods. To put it simply, the stronger your accounting foundation, the more seamless your growth journey will be, with fewer surprises and wiser business choices. Remember, you cannot do it all alone; you’ll require an eCommerce accounting expert to help & guide you towards sustainable & compliant growth.

People Also Ask:

What accounting system is best for online retailers in the UK?

With MTD compliance becoming a necessity, you need an accounting system that seamlessly integrates with your Shopify, Amazon, WooCommerce, Stripe, and PayPal, and also your inventory system. For this, Xero is the ideal choice.

However, retailers who desire sophisticated reporting and thorough spending tracking may also find QuickBooks Online to be a good choice. Your sales channels, order volume, and whether you want robust inventory management integrations will ultimately determine which solution is best for you.

Why is inventory accounting so important for online retailers?

For online retailers, inventory accounting is crucial since it maintains COGS and profit margins accurately. Without it, your taxes could be incorrect, your financial reports could be deceptive, and you could lose money due to dead stock, shrinkage, or overbuying.

Do online retailers need to register for VAT?

Indeed, depending on their sales, online shops might need to register for VAT.

You have to register for VAT in the UK if:

– In any rolling 12-month period, your VAT-taxable turnover surpasses £90,000.

– In the next thirty days, you hope to surpass it.

Some internet shops decide to voluntarily register even below the threshold (for example, to recover VAT on expenses); however, it’s not always advantageous.

How often should online retailers reconcile their accounts?

Due to frequent sales, refunds, and platform fee withdrawals, online businesses should preferably reconcile their accounts once a week. However, you can go for daily reconciliation if your company has a large order volume.

Can online retailers manage accounting without an accountant?

Yes, using programs like Xero or QuickBooks, online retailers can handle basic accounting without an accountant, particularly in the beginning.

However, an accountant is necessary to guarantee precise reconciliations, correct VAT/tax filings, and genuine profit tracking in order to prevent costly errors as sales increase (more orders, VAT, inventory, numerous platforms).

What records should online retailers keep for HMRC?

Online retailers should keep clear, organised records for HMRC to stay compliant and avoid penalties.

Key records to keep include:

– Sales records (invoices/receipts, Shopify/Amazon sales reports)

– Bank statements and transaction history

– Expense receipts and supplier invoices

– Marketplace and payment gateway reports (Amazon settlements, Stripe/PayPal fees)

– Refunds, returns, and chargeback records

– Inventory records (stock purchases, stock levels, COGS)

– VAT records (VAT invoices, VAT returns, MTD digital records)

As a best practice, keep records for at least 6 years, as HMRC may request them for checks or audits.