A recruitment firm was celebrating the month with the biggest growth, more contractors, placements, and income. However, the financial team was overburdened in the background. Payroll reports were inconsistent with CIS deductions, VAT files were delayed, and HMRC notices began to gather. On the surface level, it appeared successful, but on the inside, compliance stress was taking over.

It is common in construction-recruiting agencies because CIS and VAT are part of everyday payment and invoicing activities. They need to be managed throughout the process, not handled as separate tasks at the end. Without a clear framework, things can go out of control. In this blog, we will go over important payroll issues, CIS and VAT for recruitment agencies’ compliance, and how to streamline procedures for more efficient operations and improved financial management.

See what specialist payroll costs for your agency in seconds. Then find out if your payroll is actually compliant.

What is CIS and How It Applies to Recruitment Agencies

Contractors and subcontractors employed in the construction industry are subject to the Construction Industry Scheme (CIS), an HMRC tax system, where contractors deduct tax at source from subcontractor payments and send it straight to HMRC.

Because many contract or temporary workers may be subject to CIS regulations rather than regular payroll, CIS becomes extremely important for recruitment firms, which offer labour to construction companies.

How CIS Works in the Recruitment Context?

Workers hired by your recruitment agency may be considered subcontractors under CIS if they work for construction firms. In other words, the client (contractor) reports the tax to HMRC after deducting it from their payment.

Example: A building company receives a scaffolder from a recruitment agency. The scaffolder may not be paid in full; instead, CIS tax (often 20% or 30%) may be subtracted.

When Temp Staff Fall Under CIS

Temp or contract staff may fall under CIS when:

- They are working on construction-related activities (e.g., site work, demolition, repairs, installations)

- They are engaged as self-employed subcontractors rather than employees

- The end client is a registered CIS contractor

Many of these placements are also paid on a weekly cycle, which brings its own admin pressure on top of CIS — see our guide on managing weekly payroll for temp and contract staff.

CIS vs Standard Payroll (Key Differences)

CIS Payroll:

- Applies to self-employed subcontractors in construction

- Tax is deducted at source by the contractor

- No employee benefits, like PAYE tax codes or NIC contributions, are handled in the same way

- Focuses on payments between contractor and subcontractor

Standard Payroll (PAYE):

- Applies to employees on the agency payroll

- Employer calculates paye and deducts tax, NI, and pension contributions

- Employees receive a net salary after deductions

- Includes full employment rights and reporting obligations

Getting this classification right matters beyond CIS — misclassifying a worker as self-employed when IR35 rules say otherwise carries its own HMRC risk. Our guide to IR35 and umbrella legislation changes from April 2026 breaks down what agencies placing contractors need to prepare for.

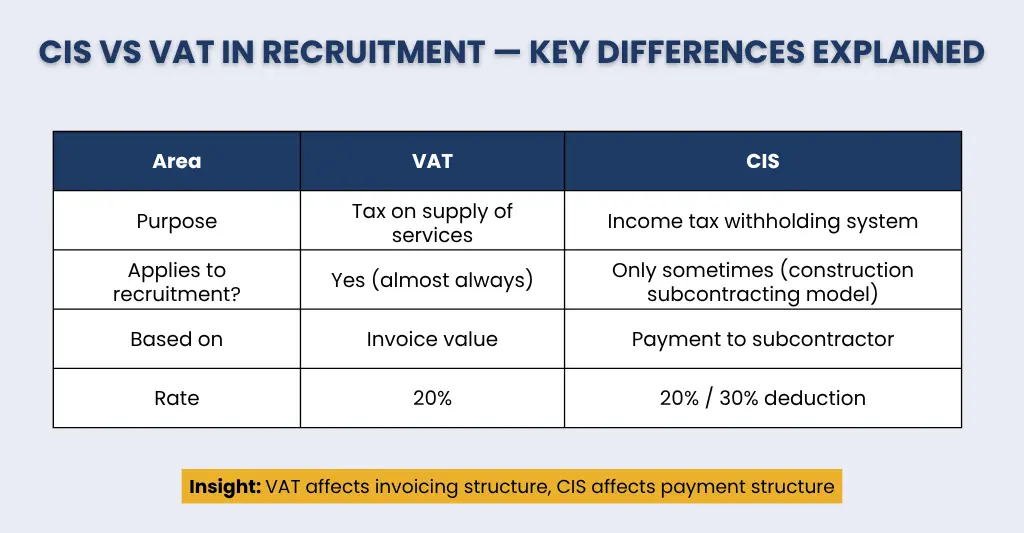

VAT Considerations for Recruitment Agencies

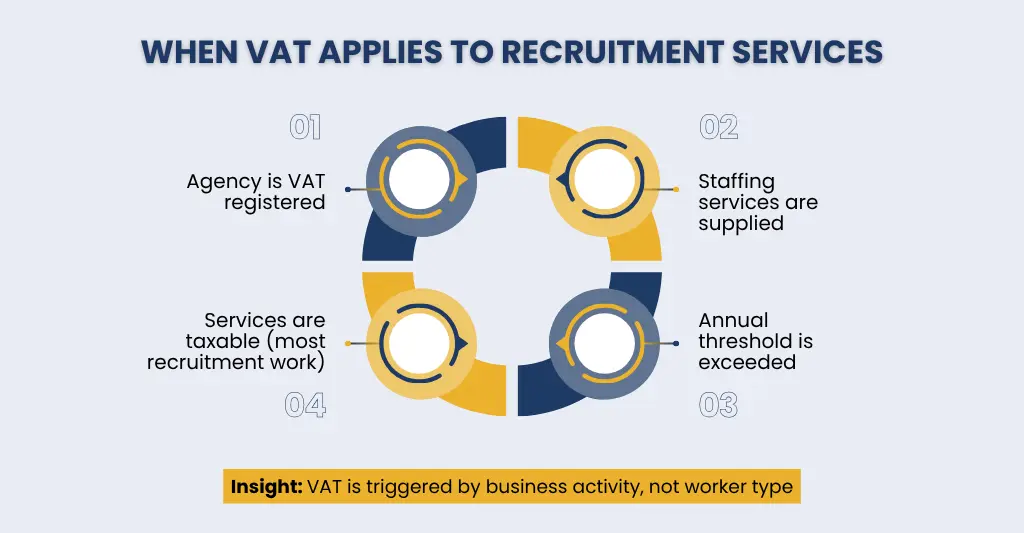

When VAT applies to agency invoices

Invoices from recruiting agencies that are VAT-registered and whose services fall under the category of taxable supplies in the UK are subject to VAT.

Recruitment firms are typically required to include VAT on their invoices when they:

- Provide temporary or permanent staffing services to clients

- Exceed the VAT registration threshold set by HMRC

- Supply services that are not VAT-exempt (which include most recruitment services)

Example:

If a recruitment agency places a temporary worker with a client and charges a £1,000 placement or staffing fee, it will typically add 20% VAT, making the total invoice £1,200.

Domestic reverse charge – brief explanation

In the UK construction industry, the Domestic Reverse Charge (DRC) is a VAT accounting method where VAT is recorded by the customer rather than the supplier. The contractor or end client is now responsible for declaring both output and input VAT on their VAT return, rather than the subcontractor charging VAT on their invoice. This eliminates the possibility of supply chain VAT fraud.

Why it matters for recruitment agencies

Depending on how services are planned, the DRC may become important for recruitment firms that provide temporary workers for labour-only subcontracting or building projects.

- The invoice may need to be handled under the reverse charge rules instead of ordinary VAT charging if an agency provides labour to VAT-registered construction companies and the service is classified as construction services under CIS regulations.

- In order to determine VAT treatment, agencies must evaluate if they are functioning as a labour supplier or a subcontractor middleman.

- Inaccurate VAT treatment may result in HMRC fines, underpaid VAT, and compliance problems.

In order to accurately determine when the Domestic Reverse Charge applies and when ordinary VAT regulations should be applied, recruitment firms that work with construction customers must thoroughly examine contracts and supply chains. Getting this assessment right from the outset is exactly the kind of contract-by-contract review our VAT services team carries out for recruitment clients working across construction supply chains.

If payroll itself feels like the bigger bottleneck day to day, our guide on optimising payroll for recruitment agencies covers the operational side of this in more depth.

Managing CIS and VAT Together

CIS (Construction Industry Scheme) and VAT duties frequently coexist for recruiting firms that engage with construction clients, and properly handling both is crucial to avoiding cash flow problems and HMRC fines.

While VAT controls how tax is charged on invoices and submitted to HMRC, CIS controls how payments to subcontractors are taxed at source. The interaction of both systems presents a problem for agencies, particularly when labour supply, subcontracting chains, and the Domestic Reverse Charge are involved.

How a company should invoice VAT and CIS

Correct invoicing under VAT and CIS regulations is essential for recruitment firms working in the construction industry in order to maintain compliance and prevent payment delays or HMRC problems. The structure of an invoice is determined by whether VAT, CIS deductions, or both (including the Domestic Reverse Charge) are applicable.

- Start with a clear breakdown of labour and materials:

Invoices should clearly separate:- Labour charges (usually subject to CIS)

- Materials (typically not subject to CIS deductions)

- Any additional reimbursable costs, if applicable

Because CIS deductions are only applied to the labour portion and not the materials, this split is crucial.

- Apply CIS deduction where required:

If the agency is supplying subcontractors under CIS:- Deduct CIS at the correct rate (20% or 30%)

- Show the deduction clearly on the invoice or payment statement

- Pay the net amount to the subcontractor

- Report the deduction to HMRC via CIS returns

In order for subcontractors to understand precisely how the deduction was computed, transparency is crucial.

- Determine the correct VAT treatment:

The structure of the supply determines VAT:- Standard VAT: If standard VAT regulations are in effect, apply VAT on the taxable amount following CIS treatment (if applicable).

- Domestic Reverse Charge: Do not charge VAT while providing building services between enterprises that are registered for VAT. Rather, add a remark like “Reverse charge: customer to account for VAT to HMRC.”

- Standard VAT: If standard VAT regulations are in effect, apply VAT on the taxable amount following CIS treatment (if applicable).

- Include mandatory invoice wording:

Depending on the scenario, invoices should include:- CIS deduction statement (if applicable)

- VAT registration number

- Reverse charge wording (if applicable)

- Clear net payable amount after deductions

Software Solutions for Recruitment Agencies

Manual CIS and VAT management can result in mistakes, compliance issues, and more administrative labor, particularly for recruitment firms managing numerous contractors and intricate invoicing arrangements. Using accounting and payroll software can help you to cut down on errors and administrative time.

Accounting software with CIS and VAT support

Accounting software that supports both VAT and CIS makes compliance easier by handling both tax responsibilities on one platform. VAT calculations can be automated, CIS deductions can be tracked, compliant invoices can be generated, and correct reports can be prepared for HMRC submissions using softwares like Xero, QuickBooks, Sage, and FreeAgent. These software will decrease manual efforts, minimise errors, enhance financial visibility, and help guarantee that CIS and VAT obligations are fulfilled effectively and on schedule for recruitment firms managing numerous contractors and intricate billing arrangements.

Read our article to find out more about choosing the ideal accounting software for your company: How to Select the Best Option for Your Agency: Accounting Software for Recruitment Firms.

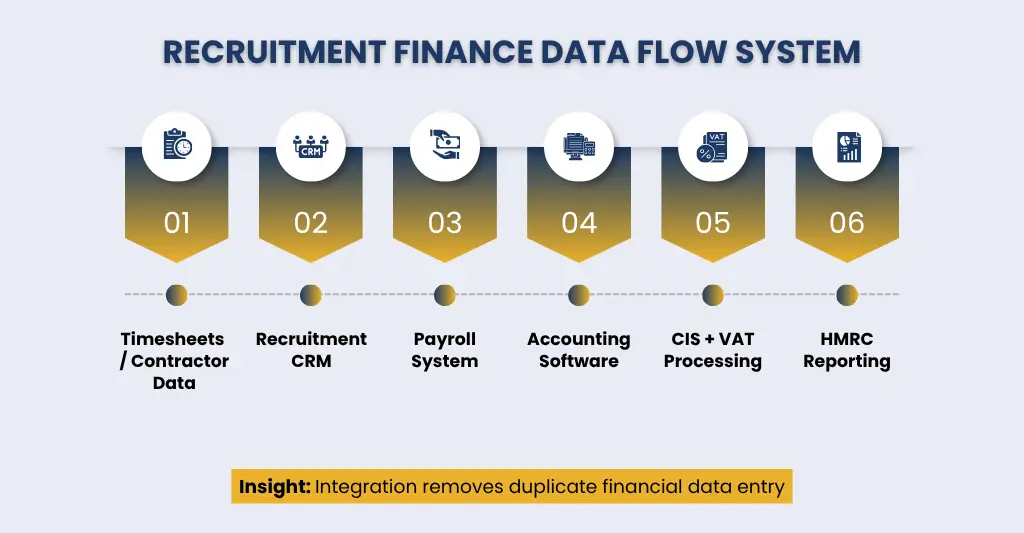

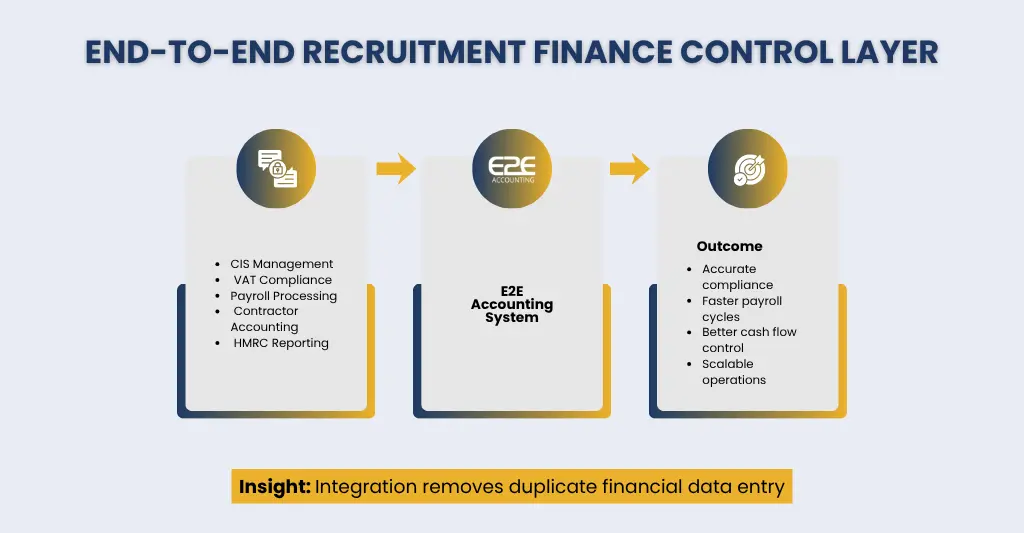

Why does integration matter?

The process of integrating your accounting, payroll, hiring, and compliance software to enable automatic data sharing between systems is known as integration. Integrated platforms synchronise contractor records, invoices, payroll data, CIS deductions, and VAT transactions in real time instead of repeatedly entering the same information.

Xero, QuickBooks, Sage, payroll software, and recruitment management platforms are just a few of the options that have built-in connectors or API connections that make these procedures easier.

How Does Integration Work?

Your accounting, payroll, and recruitment applications are connected through integration, allowing data entered into one system to be automatically updated in the others. For instance, contractor hours entered into a recruitment platform can go straight into accounting and payroll software, where invoices, VAT computations, and CIS deductions are produced immediately. This enhances accuracy, minimises manual data entry, and maintains current financial records.

Benefits of Automated Compliance Tools

- VAT obligations and CIS deductions are computed automatically.

- Lowers the risk of compliance and manual errors.

- Produces precise records for reporting to HMRC.

- Reminders for payments and filing deadlines are sent.

- Keeps an audit trail to make record-keeping simpler.

- Automates tedious administrative chores to save time.

- Increases the accuracy of tax reporting, invoicing, and payroll.

- Assists hiring firms in maintaining compliance as they grow.

Conclusion

Recruitment agencies may find it difficult to manage CIS and VAT simultaneously, especially when handling several contractors, intricate invoicing structures, and strict HMRC compliance standards. To prevent reporting errors, cash flow problems, and possible fines, it is crucial to comprehend how the two systems work together.

Agencies can decrease administrative overhead and increase accuracy by putting in place the proper procedures, utilising integrated accounting and payroll software, and automating compliance chores when feasible. Regardless of whether you are managing VAT returns, CIS deductions, or both, a proactive approach to compliance will keep your organisation productive, compliant, and growth-oriented rather than paperwork-focused. It’s also worth remembering that PAYE temp workers accrue holiday entitlement alongside their wages — our guide on how holiday pay is calculated for recruitment agencies walks through that calculation in full.

Why Choose E2E Recruitment Accountants

E2E Recruitment Accountants offer specialised accounting services tailored to recruitment agencies’unique requirements. We assist organisations in precisely and effectively managing intricate financial procedures thanks to our expert team of accountants who have knowledge of CIS, VAT, contractor payroll, invoicing, and HMRC compliance. Our customised help guarantees that your accounts, tax duties, and reporting requirements are managed expertly, freeing up your time to concentrate on business expansion.

People Also Ask:

Can a recruitment agency be CIS registered and VAT registered at the same time?

Sure. If a recruitment agency satisfies the conditions for both schemes, it can register for both VAT and CIS simultaneously. While VAT registration is applicable depending on sales or business structure, CIS registration is required when paying or working with subcontractors in the construction industry. One does not rule out the other because they operate separately.

How should a recruitment agency invoice VAT and CIS correctly?

A recruitment agency should report to HMRC, apply a CIS deduction (20% or 30%) on labor, and properly divide labor and materials. After that, VAT is either handled under the Domestic Reverse Charge, in which case the client accounts for VAT, or it is charged normally. For compliance, the invoice must clearly display the VAT treatment and CIS deduction.

Do temporary staff fall under CIS?

If temporary employees are paid through PAYE or an umbrella company, they often do not fall under CIS. Only if they are truly independent contractors working on construction projects is CIS applicable.

What deductions should a recruitment agency make for CIS?

Under CIS, a recruiting agency is required to withhold 20% (for registered subcontractors) or 30% (for unregistered subcontractors) from the labor share of compensation. Materials are not deducted, and the amount that is deducted needs to be reported and paid to HMRC.

What is the domestic reverse charge and does it affect recruitment agencies?

A VAT law known as the Domestic Reverse Charge (DRC) allows the customer to pay VAT directly to HMRC rather than having the provider charge it. Recruitment agencies may only be impacted when VAT-registered enterprises supply labor connected to construction. It doesn’t apply in the majority of PAYE staffing circumstances.

How can recruitment software help manage CIS and VAT?

By automating CIS deductions, applying accurate VAT (including reverse charge), and coordinating everything with HMRC reporting, recruitment software aids in the management of CIS and VAT. It expedites payroll and invoicing and lowers errors.

What penalties can arise for incorrect CIS or VAT filing?

HMRC penalties, interest charges, and compliance investigations may result from incorrect CIS or VAT filing.

Late returns, inaccurate deductions, and neglecting to verify subcontractors can all result in penalties for CIS. Errors in VAT can lead to interest on past-due amounts, surcharge rates, and underpaid tax penalties, particularly under Making Tax Digital regulations. Repeated errors may result in HMRC audits in extreme circumstances.

Can subcontractors working through an agency use their own CIS registration?

Sure. If a subcontractor is truly self-employed, they may use their own CIS registration. The typical deduction for registered subcontractors is 20% rather than 30%. CIS does not apply if they are on PAYE or umbrella.