Navigating employee benefits can be challenging, but a well-designed salary sacrifice scheme might be a game-changer for UK firms in 2026. These plans not only save employees money, but they can also help businesses cut National Insurance contributions, increase employee retention, and make your company more appealing to top talent.

However, with changing tax laws, compliance requirements, and a wide range of perks available, from pensions to cycle-to-work programs, understanding how to set up and administer a salary sacrifice scheme is critical. This guide explains what all employers need to know about wage sacrifice in today’s UK workplace, how to avoid mistakes, and how to maximise its benefits.

What Is a Salary Sacrifice Scheme?

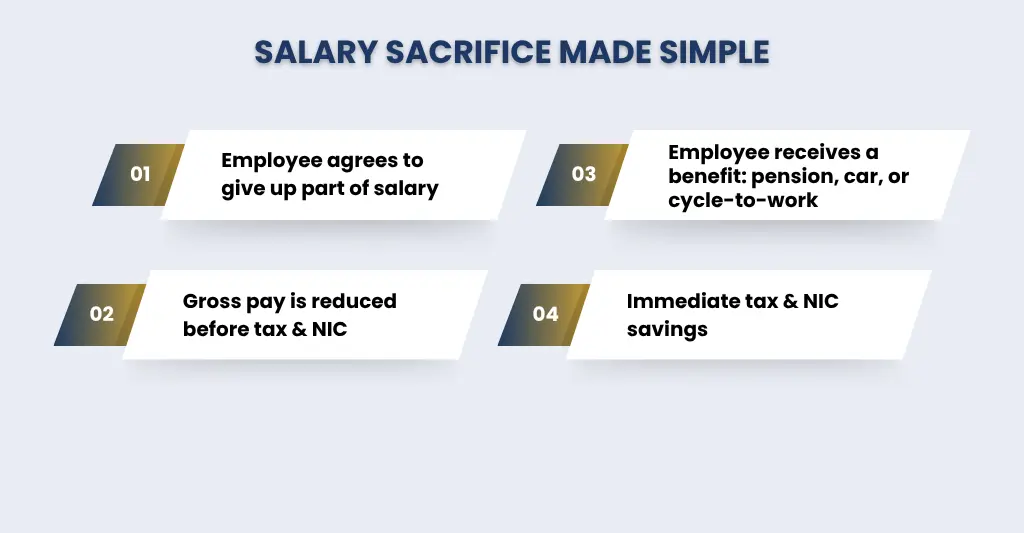

Salary sacrifice occurs when you and your employees agree to give up a portion of their compensation for something that will benefit them. So, instead of getting that money in their monthly paycheck, they will get something more important!

The great thing about salary sacrifice is that it is not taxable!

It not only decreases their income tax but also their National Insurance contributions. And the best part? Employees are not required to claim any tax relief from HMRC because the savings are made immediately.

How Salary Sacrifice Works for Employers?

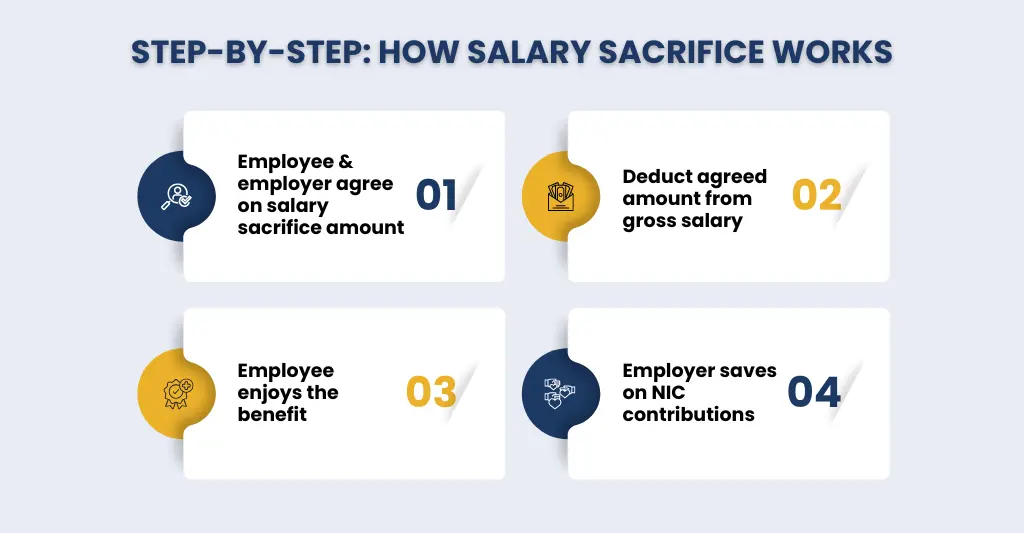

Salary sacrifice schemes are actually super simple. Here are the steps involved:

- Agreement: You must first join up with a partner who specialises in the salary sacrifice scheme of your choice. You and the employee must agree on the amount of salary they will give up in exchange for these specific advantages.

- Salary reduction: The agreed-upon sum is deducted from the employee’s monthly gross compensation before tax and national insurance contributions are computed. Because the salary sacrifice is not taxed, both you and the employee will save money on the payments.

- Receiving the benefit: Once all of the agreements are signed, you are ready to go, and employees will be able to use the benefit. Employees can take their business car for driving, buy their dream home, or start saving for retirement!

For example: Emma, who works for a marketing company, decides to acquire a new electric car through a salary sacrifice plan. She consents to forfeit £200 of her pay each month. Her taxable income is reduced because this sum is subtracted before taxes and national insurance. Emma’s workplace also benefits from decreased National Insurance contributions. She may now drive while saving money on taxes.

It is crucial to remember that there are some limitations on the kind of benefits that can be granted through salary sacrifice schemes, such as automobiles and pensions, which might sometimes have additional limits. Furthermore, not all employees will be eligible for salary sacrifice, as deductions must not lower the employee’s compensation below the national minimum wage. Salary sacrifice may affect the employee’s right to certain benefits, such as statutory sick leave or redundancy compensation.

Tax and National Insurance Rules Employers Must Follow

Salary sacrifice plans can be extremely tax-efficient, but only if they are properly set up and managed. To maintain compliance and prevent unexpected tax bills or fines, UK employers must adhere to the tight guidelines established by HM Revenue and Customs.

Optional Remuneration Arrangements (OpRA):

OpRA guidelines apply to the majority of salary sacrifice schemes. This means:

- The taxable value is determined by whichever is higher: salary sacrificed or advantage obtained

- Many perks have lost their tax advantages due to these rules.

Exceptions (still tax-efficient):

- Employer pension contributions

- Cycle to Work schemes

- Ultra-low emission vehicles (ULEVs)

For Example, Emma decides to use a salary sacrifice scheme to get a new ultra-low emission electric car. She gives up £3,000 of her salary for the car. Normally, OpRA would check which is higher: the £3,000 she gave up or the car’s value.

(If the car is worth £2,500 but Emma gave up £3,000 in salary → taxable value = £3,000).

(If the car is worth £3,500 but Emma gave up £3,000 → taxable value = £3,500.)

Because the car is tax-exempt under OpRA rules, she pays less income tax. The salary she sacrificed is fully tax-efficient, saving her money.

Impact on Income Tax:

When structured properly:

- Employees pay lower income taxes since their gross salary is reduced.

- However, for non-exempt benefits under OpRA, tax may still apply on the larger amount.

For Example: Emma gives up £200 of her salary to get a company laptop that costs £180. Because laptops are not tax-exempt, the government still treats the £200 as taxable income. So, she doesn’t save any income tax in this case.

Exempt benefit (like a pension contribution):

Instead, if Emma gives up £200 of her salary to pay into her pension, this money will be tax-free. Now her taxable salary is lower, so she has to pay less income tax. She ends up saving money simply by redirecting her salary into a benefit that is exempt.

In simple terms:

- Salary sacrifice works best when the benefit is tax-exempt.

- Giving up salary for non-exempt benefits will not give the benefit of reducing your tax, even though it might feel like “saving money.”

Quick tip: Always check whether the benefit you are getting is exempt under OpRA rules before joining a salary sacrifice scheme.

National Insurance Contributions (NICs) Savings:

One of the greatest benefits for employers.

Employer NICs are reduced as employee gross compensation is decreased. Savings could be reinvested into employee benefits or business growth. Depending on the scheme structure, employees may be able to save money on their own NICs.

Minimum Wage Compliance:

This is where many employers are caught off guard. Salary sacrifice cannot lower compensation below the National Minimum Wage (NMW). This applies following the wage reduction. Failure to follow this guideline can result in penalties and back payments.

Example: Every month, Emma makes £1,500. Through a salary sacrifice plan, she consents to donate £400 of his pay for a business vehicle. Her take-home pay would be £1,100 after the sacrifice.

This agreement is illegal if the National Minimum Wage for her working hours is £1,200. In addition to paying the difference, the employer can be subject to fines.

Reporting and Payroll Requirements:

Employers must ensure accurate reporting:

- Benefits must be reported via P11D (unless payrolled)

- Payroll systems should reflect the adjusted salary and benefits correctly

- Keep clear documentation of employee agreements

Pension and Statutory Pay Considerations:

Salary sacrifice can affect:

- Statutory payments (e.g., maternity, sick pay)

- Borrowing capacity (as official salary is lower)

Best practice: clearly communicate these impacts to employees before implementation.

Example: Emma agrees to sacrifice £300 of her monthly pay in exchange for a Cycle to Work program.

- Her official income is now less than what was used to determine statutory payments (such as maternity pay).

- Maternity pay may be less than anticipated as a result.

- Additionally, Emma’s borrowing ability would seem diminished if she files for a mortgage.

Employers should thus provide a thorough explanation of these implications prior to initiating the program.

Which Benefits Still Qualify for Tax Efficiency?

According to the most recent HM Revenue and Customs guidelines, the following benefits remain tax-efficient for 2026:

- Pension Contributions: Employer contributions made through salary sacrifice remain totally exempt from income tax and NICs.It’s often the most popular and effective option for both employees and companies.

- Cycle-to-Work Schemes: The use of bicycles while going to work is tax-free. As it encourages sustainable travelling while staying exempt from OpRA taxes.

- Ultra-Low Emission Vehicles (ULEVs): Electric or hybrid cars emitting minimal CO₂ can offer both tax and NIC savings, as they are environmentally friendly. It also creates awareness among the employees to be responsible citizens.

- Other Employer-Supported Schemes (Limited Cases): Some childcare vouchers and work-from-home supplies may still be partially exempt. To ensure compliance, always refer to current HMRC instructions.

Can Salary Sacrifice Reduce Pay Below the National Minimum Wage?

One of the most significant compliance criteria for UK firms is to ensure that salary sacrifice does not drop the salary of an employee below the National Minimum Wage (NMW). Failure to follow this requirement may result in HMRC penalties and back payments.

How Does It Work?

- Salary sacrifice lowers gross compensation in return for perks.

- The employee’s residual compensation after the sacrifice must meet or exceed the NMW or National Living Wage (NLW) for their age bracket.

- This estimate should take into account all hours worked, including overtime, to avoid accidentally underpaying employees.

How Do Employers Report Salary Sacrifice to HMRC?

Salary sacrifice arrangements are reported by employers to HMRC via the payroll system. The employee’s taxable income is decreased by deducting the sacrificed amount from their gross wage before tax and National Insurance contributions are calculated.

Employers then include the modified salary amounts for the majority of salary sacrifice benefits (note: there can be more than one benefit at the same time) on the employee’s P60 at year-end and in the Full Payment Submission (FPS).

Non-cash or taxable perks, like a company car or private health insurance, must be reported on Form P11D.

What Evidence Should Employers Retain?

Employers should maintain clear records showing how the scheme operates, including employee agreements and any calculations. Saving all documents is essential for HMRC compliance and to protect the company if audits or disputes arise.

Employee Agreements:

- Each participating employee must give their written consent or sign agreements.

- Salary details prior to and following the sacrifice.

- A clear explanation of the benefit and its cash equivalent.

Payroll Records:

- Documentation of gross salary modifications for each pay period.

- Income Tax and National Insurance Contribution deductions based on lower salaries are to be recorded.

- Evidence showing wages did not fall below the National Minimum Wage.

Benefit Documentation:

Proof of the benefit provided (for example, pension payments, cycle-to-work equipment, or ultra-low emission automobiles), Invoices, receipts, or contracts regarding the scheme.

Reporting Evidence:

- Copies of P11D forms or payrolled benefits reports submitted to HMRC.

- Records of Class 1A NICs paid where applicable.

Compliance Checks: Internal audits or reviews validate that scheme rules were followed. Take notes on any communications to employees that clarify statutory pay, pension contributions, or the NMW impact.

Workplace Pension Salary Sacrifice Schemes

In the United Kingdom, workplace pension contributions are one of the most prevalent and tax-efficient types of salary sacrifice. When properly organised, these plans let employees trade a portion of their pay for higher pension contributions, providing significant financial benefits to both employees and employers.

- Employee Agrees to Sacrifice Part of Salary: An employee decides to cut their gross income by a certain amount or percentage. This reduction is to be fully agreed and documented.

- Example: Emma earns £35,000 per year and agrees to sacrifice £2,000 for her pension:

- Her taxable salary drops to £33,000.

- She pays less Income Tax and NICs.

- The employer also saves NICs on the £2,000 contribution.

- Benefits for Employees: Increases retirement savings without affecting net income as much as a direct contribution. Reduces income tax liability for the sacrificed amount. NIC savings frequently increase overall take-home earnings.

- Benefits for Employers: Reduces employer NICs for participating employees. Offers competitive pension benefits to encourage employee retention. Supports adherence to auto-enrolment rules under UK pensions law.

- Example: Emma earns £35,000 per year and agrees to sacrifice £2,000 for her pension:

- Compliance Considerations: Employers must ensure:

- Agreements are documented clearly for each employee.

- The reduced salary does not fall below NMW/NLW.

- Payroll systems correctly reflect the sacrificed salary and pension contribution.

- Reporting to HMRC is accurate, particularly if contributions are payrolled.

Pros and Cons of Salary Sacrifice for Employers

Salary Sacrifice Scheme can be a useful tool if it’s used correctly, but it also has certain advantages and disadvantages. Understanding both sides is necessary so you can decide whether the scheme will work for you or not.

Pros:

- National Insurance Savings: Employer NICs are calculated based on lower gross incomes, which means that businesses pay less NICs to participating employees.

This can result in significant cost savings, particularly for higher-paid employees.

- Enhanced Employee Benefits: Providing programs such as pensions, cycle-to-work, and ultra-low emission vehicles makes your organisation more impressive to stakeholders or clients. It also increases staff retention and satisfaction.

- Tax Efficiency: Employees pay less in income tax and national insurance contributions on the sacrificed compensation, leading to a win-win situation. Employers can profit from increased total labour involvement with benefits programs.

- Supports Corporate Responsibility Goals: Schemes such as cycle-to-work and ULEVs promote sustainable transportation. Shows a company’s dedication to protecting the environment and staff well-being.

- Flexibility: Employers can pick which benefits to provide, adapting plans to specific teams or employee needs.

Cons:

- Compliance Risks: Salaries must not fall below NMW/NLW. Non-compliant programs may result in HMRC penalties and back payments.

- Payroll Complexity: Payroll systems must appropriately record salary reductions, benefit values, and NIC savings. Errors might result in improper pay, statutory payment miscalculations, or reporting problems.

- Impact on Statutory Payments: To be in compliance, you must document, retain records, and conduct regular audits. NMW/NLW rates and HMRC rules may change, necessitating changes.

- Limited Tax Advantage for Some Benefits: Non-exempt rewards under OpRA rules (Optional Remuneration Arrangements) may still be taxed, diminishing the perceived benefit.

How to Set Up a Salary Sacrifice Scheme (Employer Checklist)

Setting up a salary sacrifice arrangement in 2026 takes careful planning to ensure compliance and maximise advantage. Here is a concise checklist:

- Choose Benefits: Provide tax-efficient benefits such as pensions, cycle-to-work programs, or ultra-low-emission vehicles.

- Check Eligibility: Ensure employees’ reduced salary stays above NMW/NLW.

- Get Agreements: Document employee consent, salary changes, and benefit details.

- Update Payroll: Recognise salary reductions, NIC adjustments, and statutory pay accurately.

- Report to HMRC: Payrolled benefits via payroll; others via P11D/P11D(b).

- Communicate Clearly: Explain the impact on take-home pay, pensions, and statutory payments.

- Monitor & Review: Keep scheme updated with NMW/NLW changes and HMRC guidance.

- Keep Records: Maintain all agreements and payroll records for at least six years.

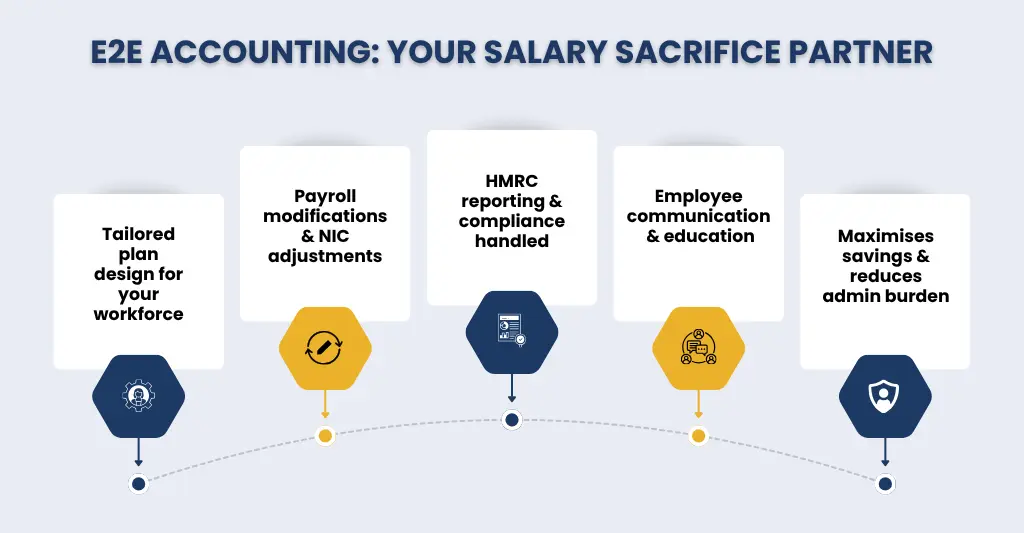

Why Choose E2E Accounting UK for Salary Sacrifice Implementation?

E2E Accounting UK makes implementing salary sacrifice schemes straightforward, compliant, and stress-free for employers. With extensive knowledge of UK payroll, pensions, and HMRC rules, we can handle everything from plan design and payroll modifications to reporting and employee communications. Our staff ensures that each program maximises tax and NIC savings, remains fully compliant with 2026 laws, and is personalised to your workforce, allowing you to offer appealing benefits without the administrative effort or danger of errors.

Contact E2E for customised payroll services today, and let both parties reap the benefits while staying compliant.

People Also Ask:

Is salary sacrifice legal in the UK?

Yes, salary sacrifice is completely legal in the UK if planned correctly. Employers must ensure that the reduced salary does not fall below the National minimum wage and that benefits are reported to HMRC according to current tax rules.

Does salary sacrifice reduce employer National Insurance?

Yes, by reducing an employee’s gross salary, salary sacrifice reduces the amount of employer National Insurance Contributions (NICs) payable – making it a cost-efficient option while ensuring full compliance.

Can employees opt in and out anytime?

No, employees are not allowed to withdraw or change from a salary sacrifice scheme as per their choice. Opt-in and opt-out rules must be agreed in advance, and changes are mostly allowed during specific periods or with employer consent to ensure compliance and accurate payroll processing.

Is salary sacrifice worth it?

Yes, it is beneficial to both the employer and the employee. Employees can save on income tax and National Insurance. This boosts take-home salary or pension contributions for employees. Whereas, employers benefit from reduced NICs and staff retention.

Are salary sacrifice car schemes worth it?

They can be, but it depends on the type of vehicle and the tax requirements. Ultra-low emission vehicles (ULEVs) are typically the most tax-efficient, saving on income tax and NICs. Older or higher-emission vehicles may provide less or no advantages, thus careful planning is required to make the project worthwhile.

Does salary sacrifice affect mortgage applications?

Yes, due to the salary sacrifice scheme, gross income is reduced, so lenders see a low amount of salary while assessing the affordability of the applicant. Therefore, employees should disclose the sacrificed amount during mortgage applications, as it may affect the borrowing limit or approvals.

Can directors use salary sacrifice?

Yes, company directors can participate in salary sacrifice schemes, but proper strategic planning is needed. Reducing their gross payments may have an impact on National Minimum Wage standards, statutory payments, and pension contributions, so planning must be properly done to be compliant and advantageous.