The Tale of Two Landlords

Arthur and Eleanor both owned property in the heart of Bristol, but that is where the similarities ended.

Arthur was a traditionalist. He owned three mid-terrace Victorian houses, which he rented to reliable, long-term professional families. To Arthur, property management was a slow and steady game of patience.

In contrast, Eleanor was an aggressive modern strategist. She operated a portfolio of high-yield seaside apartments and city centre flats listed exclusively on Airbnb and VRBO. Her properties were revolving doors for weekend tourists, corporate travellers, and digital nomads.

Both were highly successful on paper, generating thousands of pounds in monthly revenues. However, as the dreaded January self-assessment deadline loomed, their realities diverged drastically.

Arthur spent his evenings buried under mountains of faded shoe-box receipts, desperately trying to calculate what he owed to HM Revenue & Customs (HMRC), paralysed by the fear of an audit. Eleanor sat calmly in a local coffee shop, scrolling through clean, real-time financial dashboards on her phone and knowing exactly where every penny stood.

The difference? Eleanor had discovered how to master accounting for rental property, transforming her finances from a chaotic chore into a strategic weapon. Arthur was still treating his investments like an amateur hobby.

Whether you align with Arthur’s traditional approach or Eleanor’s fast-paced short-term model, this guide will walk you through the exact blueprint required to conquer your real estate books, maximise your tax efficiency, and achieve true financial peace of mind.

How to Do Accounting for Rental Property

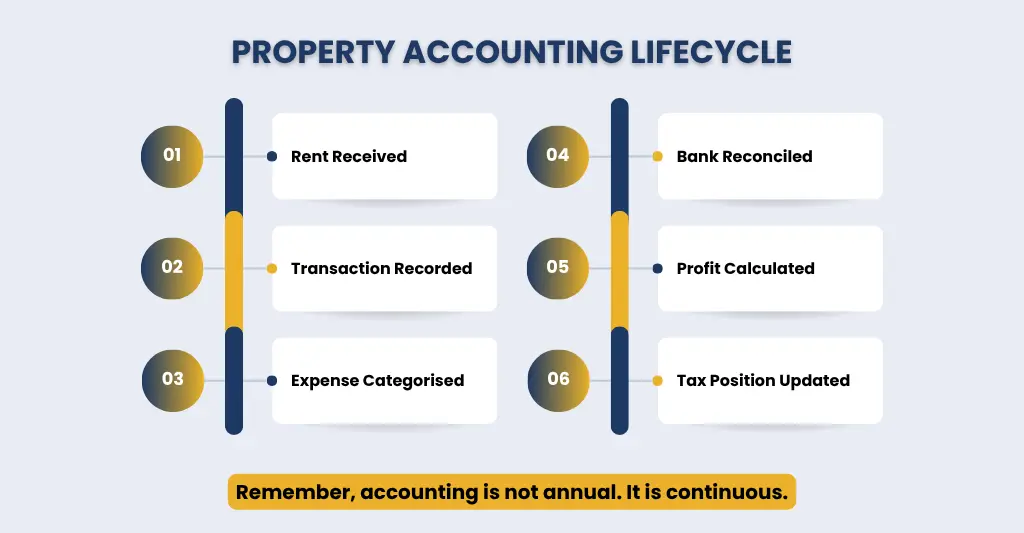

Many property investors view accounting for rental property as a post-facto obligation—something that is frantically assembled at the end of the financial year to satisfy the taxman. This is a fundamental error.

Learning “how to do accounting for rental property” involves establishing a continuous, live operational loop. It is a systematic process of recording, classifying, summarising, and interpreting every financial transaction related to real estate assets.

To build a structurally sound property ledger, every pound sterling must be viewed through a dual lens:

[Inflow: Total Cash Received] — [Outflow: Allowable Operational Costs] = Net Taxable Profit

Every rent payment, maintenance invoice, furniture replacement, and insurance premium must be tracked with absolute accuracy.

For UK property owners, this is regulated by the strict guidelines and principles of the UK tax law and HMRC. You need to have a tight bookkeeping system, from manual books to complicated spreadsheets or a cloud-based program, that records money at the moment it is received.

If you do not know where your cash flow is going, you are not investing; you are gambling.

Key Accounting Terms Every Property Manager Should Know

Before we dive into execution, we must master the vocabulary of trading. If you cannot speak the language of real estate finance, you cannot hope to manage it properly.

- Gross Rental Yield: The total annual rental income generated by a property, expressed as a percentage of its total purchase price or current market value.

- Net Rental Yield: A far more critical metric. This is your annual rental income minus all operating expenses (repairs, management fees, insurance) divided by the property value. It indicates the true earning power of an asset.

- Allowable Expenses: These are the costs incurred for running and maintaining your rental property, in connection with your rental business, and which are “wholly and exclusively” for the rental business. These are claimable directly from the gross income and reduce the taxable profit in the company tax return.

- Capital Expenditures (CapEx): These are funds used for the purchase of structural improvements or enhancements to a property (such as a new rear extension or a brand-new loft conversion). These are not tax-deductible in the income tax year but may be used to offset Capital Gains Tax (CGT) at the time of the sale.

- Section 24 (Finance No. 2 Act 2015) changed how mortgage interest relief works for individual landlords. Instead of deducting mortgage interest from rental income before tax, landlords now receive only a 20% tax credit on finance costs, increasing taxable income and often pushing some landlords into higher tax bands.

You can also explore legal tax planning strategies for self-employed and property investors to optimise your liabilities.

- Accrual Accounting vs. Cash Basis Accounting: Cash basis is when you recognise income and expenses at the time you receive or spend the actual cash. Accrual accounting recognises a transaction as an earning or an invoice, even if the cash has not yet changed hands. (HMRC allows a cash basis for landlords with income from renting of less than £150,000 per year). Learn more about how accruals and prepayments work in practice in our complete UK SME guide

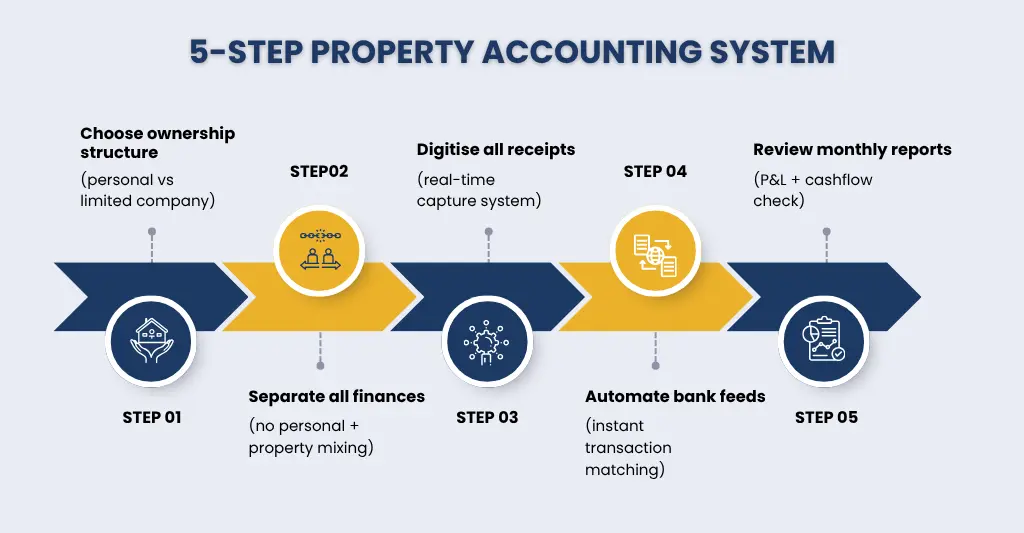

Practical Steps To Master Accounting for Rental Property

To transition from financial chaos to total mastery while accounting for rental property, follow this chronological five-step framework.

Step 1: Establish Your Legal Vehicle

Decide whether you will hold your properties in your personal name or via a limited company. Personally held properties are subject to individual income tax rates of up to 45% and face full Section 24 restrictions. Limited companies are subject to Corporation Tax rates (ranging from 19% to 25%) and can fully deduct mortgage interest as a business expense. Explore ways to legally reduce corporation tax to make your property company even more efficient.

Step 2: Draw a Hard Line Between Personal and Corporate Funds

The absolute bedrock of property bookkeeping is isolation. You must treat your property portfolio as a completely separate living organism, entirely disconnected from your personal lifestyle.

Step 3: Implement an Immediate Cloud-Based Invoicing Protocol

Avoid delaying the repair bill until the weekend! Get a digital scanning solution to instantly photograph, classify, and store all invoices as they arrive in your inbox or in your hands.

Step 4: Automate Bank Feed Reconciliations

Link your property accounts directly to an automated ledger engine. Every time a tenant pays rent or a letting agent deducts a fee, the transaction should be auto-matched to its corresponding property unit within the system.

Step 5: Schedule Monthly Financial Audits

Take a month-end profit and loss statement (P&L) and spend 60 minutes on the first day of each month examining it. Check for irregularities: rising maintenance costs? Are there specific units that are at risk of being eroded over time?

Part 1: Accounting for Long-Term Rental Properties (Traditional Rentals)

Let us return to Arthur, our traditional Bristol landlord, for a moment. Arthur’s business model is built on stability, but his financial bookkeeping is anything but stable. He assumed that because his tenants signed 12-month Assured Shorthold Tenancies (ASTs), his accounting would be straightforward. He was wrong.

What is Long-Term Rental Property Accounting?

Long-term rental accounting focuses on tracking highly predictable recurring revenue cycles alongside intermittent property management and maintenance overheads. Because tenants remain in situ for months or years at a time, the financial goal here is long-term cash flow predictability through management accounts, rigorous tracking of tenant deposits, and precise monitoring of allowable deductions under the individual or corporate tax frameworks.

Key Accounting Tasks for Long-Term Rentals

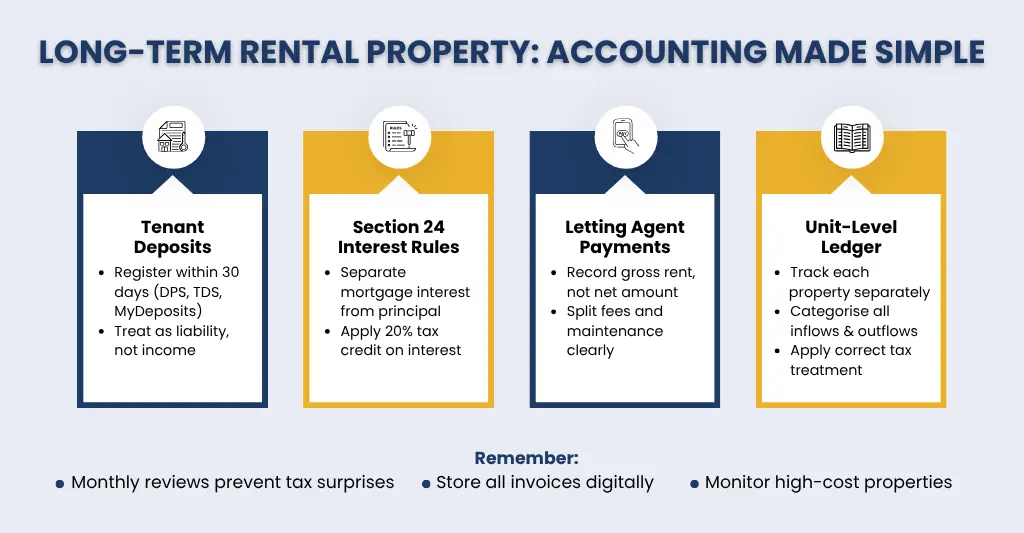

For portfolios such as Arthur’s, success comes down to mastering four primary pillars:

- Tracking and Protecting Tenant Deposits: Under UK law, tenancy deposits must be registered with a government-backed scheme (such as the DPS, TDS, or MyDeposits) within 30 days of their receipt. Your accounting records must show these funds as a balance sheet liability and not as liquid operational cash.

- Section 24 Calculation: Separating mortgage principal payments (non-deductible) from mortgage interest payments (subject to the 20% tax credit for individual owners) to avoid catastrophic year-end tax surprises.

- Managing Letting Agent Disbursals: Letting agents often collect the rent, deduct their 10–12% management fee, pay for an emergency plumber out of the gross funds, and send you the net remainder. You cannot simply log the net amount received; you must account for the full gross income and break down the agent’s fees and maintainance costs as separate expenses.

Practical Guidance (To Its Correct Accounting)

To keep a long-term portfolio structurally sound, construct a dedicated ledger that is cleanly broken down by unit. For every property, maintain an active tracking file that mirrors the following layout:

| Date | Transaction Description | Category | Inflow (£) | Outflow (£) | Tax Treatment |

| 01/05/2026 | Rent: 12 Oakfield Road | Gross Rental Income | 1,500.00 | 0.00 | Taxable Income |

| 03/05/2026 | Agent Management Fee | Professional Fees | 0.00 | 150.00 | Fully Allowable Expense |

| 12/05/2026 | Replace Broken Kitchen Tap | Property Repairs | 0.00 | 120.00 | Fully Allowable Expense |

| 15/05/2026 | Monthly Mortgage Payment | Finance Cost | 0.00 | 650.00 | Interest portion subject to 20% credit |

By forcing every transaction into this rigid format, Arthur would instantly see that his actual taxable profit is not simply the cash left in his bank account. He would be fully prepared for his self-assessment long before January.

Part 2: Accounting for Short-Term Rental Properties (Airbnb, Vrbo, etc.)

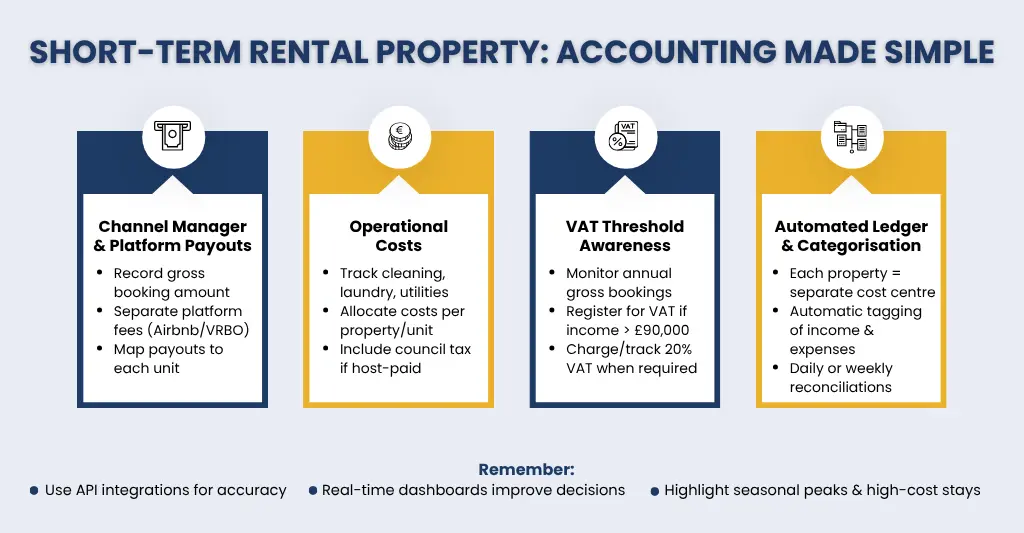

Now, let us switch perspectives to Eleanor, the short-term rental strategist. While Arthur deals with 12 transactions per property per year for rent, Eleanor deals with hundreds of transactions. Her apartments experience constant flux in guest bookings, cleaning fees, platform commissions, and seasonal pricing adjustments.

What is Short-Term Rental Property Accounting?

Short-term rental accounting is highly dynamic and has high-volume transactional bookkeeping. It requires managing micro-stays, fluid pricing models, immediate platform deductions, and specialised UK tax incentives—specifically the highly lucrative Furnished Holiday Lettings (FHL) framework (or local equivalent structures)–which grants distinct tax advantages over traditional residential lets if specific occupancy criteria are met.

Key Accounting Tasks for Short-Term Rentals

Eleanor’s daily operational ledger involves navigating unique and volatile financial variables:

- Reconciling Channel Manager Payouts: Platforms such as Airbnb collect money from guests, deduct their service fee (typically 3% to 5% or more), and transfer the net amount to your bank. Your accounting system must map the gross guest payment and platform fee separately to keep your gross turnover metrics accurate for VAT monitoring.

- Utility and Operational Overhead Allocation: Short-term rentals require the host to cover all Wi-Fi, council tax, electricity, gas, and water bills for the guest. These must be rigorously tracked as operational revenue and expenses.

- VAT Threshold Watch: Unlike residential lets, short-term holiday accommodation is considered a taxable supply for VAT purposes. If Eleanor’s gross booking income (before platform fee deductions) crosses the UK VAT threshold (currently £90,000), she must register for VAT and charge 20% on her bookings or utilise specialised accounting schemes to preserve her margins.

Practical Guidance (To Its Correct Accounting)

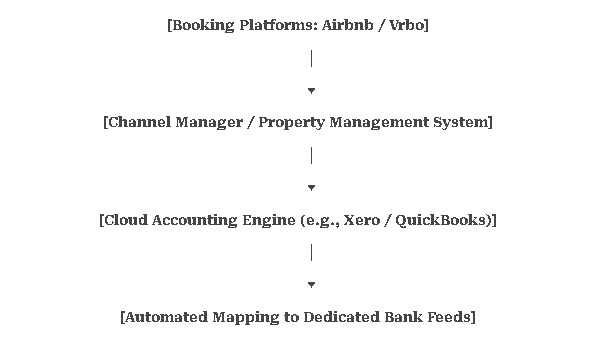

Because of the sheer volume of data, short-term property accounting cannot be performed manually without driving oneself to exhaustion.

A practical solution requires direct API integration.

Eleanor maps every listing as an individual “tracking category” or “cost center” within her cloud system. When Airbnb pays out £800 for a 3-night stay, the software automatically pulls the underlying reservation data, creating an invoice for the gross booking amount (£840) and simultaneously creating an expense for the Airbnb commission (£40).

Cleaning costs and laundry services are instantly tagged to that specific unit, providing Eleanor with a real-time daily assessment of her net holiday-let yields.

Common Accounting Mistakes to Avoid as Property Managers

Whether you run long-term lets or short-term holiday rentals, stepping into these financial traps can devastate your portfolio’s profitability and trigger severe penalties from tax authorities.

- Treating the Property Account as a Personal Piggy Bank: Withdrawing cash from the property account to buy groceries or pay for a personal holiday ruins your corporate tax history. It creates messy director’s loan complications if you run a limited company, and makes an HMRC audit incredibly painful.

- Failing to Differentiate Between Repair and Improvement: Replacing a worn-out, broken laminate floor with an identical modern laminate is a repair (revenue expense, instantly deductible). Tearing out a functional kitchen to build a luxury state-of-the-art chef’s cooking space is an improvement (capital expense, non-deductible against income tax). Claiming capital improvements as repairs to artificially depress your income tax bill is a primary target for HMRC compliance.

- Losing the Paper Trail for Cash Payments: Paying a local tradesperson in cash to fix a roof leak without securing an official, itemised invoice means that the expense effectively does not exist in the eyes of the law. You lose the tax deduction, which means you will pay significantly more tax than necessary.

- Neglecting the Making Tax Digital (MTD) Timeline: HMRC’s Making Tax Digital initiatives from 2026 mean that landlords with qualifying property income will soon be legally required to maintain digital records and submit quarterly reporting online. Continuing to rely on paper logbooks or disorganised spreadsheets will leave you completely non-compliant.

How to Streamline Your Property Management Accounting

If you find yourself drowning in financial administration, it is time to optimise your operational workflow. Institutional-grade financial streamlining can be achieved by adopting three modern strategies:

1. Go 100% Paperless with Optical Character Recognition (OCR)

Stop saving paper receipts in wallets, drawers, or glove compartments. Use mobile document capture tools, such as Dext or Hubdoc. When a contractor hands you an invoice, snap a photo. The embedded OCR technology automatically extracts the supplier name, date, invoice number, and total amount, sending the structured data directly to your digital books without a single keystroke of manual data entry.

2. Leverage Specialised Property Management Accounting Software

While general accounting platforms such as Xero, QuickBooks, or Sage form an excellent core engine, connecting them with dedicated property software ecosystems (such as Arthur Online, Hammock, or Landlord Studio) unlocks unparalleled power. These specialised tools understand real estate logic. They track tenancies, send automated rent reminders to tenants, log gas safety expiration dates, and automatically generate clean landlord statements.

3. Implement Daily or Weekly Automated Bank Reconciliations

Never let transactions accumulate over months. Spend just 10 minutes every Friday morning matching your digital bank feed to your open invoices. Keeping your books permanently reconciled ensures that your financial dashboards reflect the exact truth of your business at any given moment.

How E2E UK Property Management Accountants Can Help

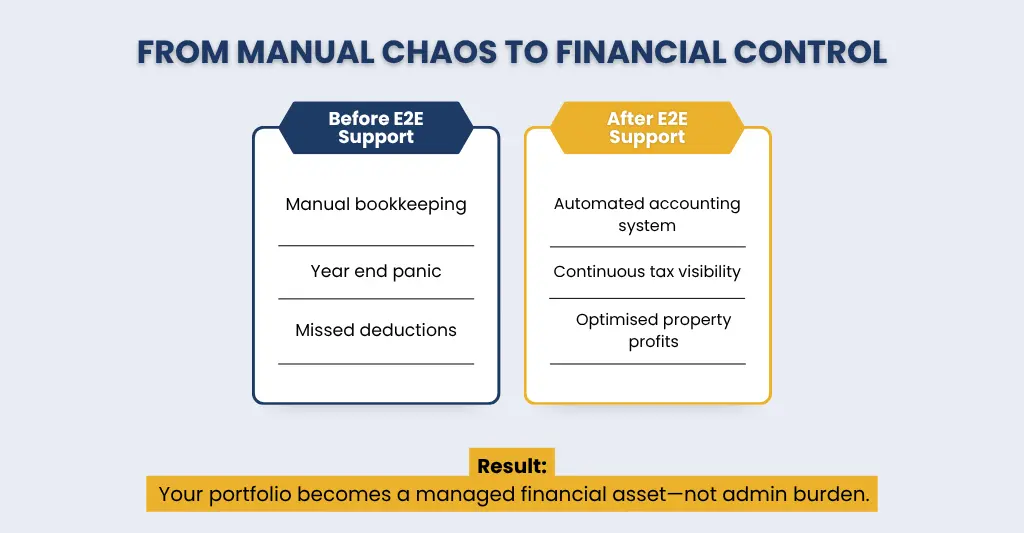

In our Bristol story, Arthur eventually reaches a breaking point. After missing an algorithmic tax deduction and facing an aggressive compliance check from the HMRC over an incorrectly categorised boiler replacement, he realised he could no longer manage his expanding financial obligations alone.

He asked himself a fundamental question: “Am I a property investor, or am I an underpaid, stressed-out bookkeeper?”

He reached out to E2E UK Property Management Accountants, a specialist accounting firm dedicated to navigating the intricacies of UK real estate taxation.

Partnering with an expert property-focused accounting firm, such as E2E, fundamentally transforms your investment journey. Here is how they can help you master your portfolio:

- Comprehensive Portfolio Restructuring: We at E2E will analyse your portfolio to establish whether restructuring it into a limited company structure (incorporation) will protect you from Section 24 tax penalties and maximise your net cash flow.

- Flawless Making Tax Digital (MTD) Migration: We help you move your old books, spreadsheets, and shoeboxes into state-of-the-art MTD-compliant business, so you are always protected against future MTD changes.

- Advanced Holiday Let & VAT Navigation: For short-term hosts like Eleanor, E2E manages complex VAT registration options, monitors FHL guidelines, and ensures that platform fees are optimised to protect profit margins.

- Proactive Forensic Tax Planning: Instead of simply telling you what you owe after the year has ended, E2E works with you proactively throughout the cycle to uncover every single legitimate allowable expense, capital allowance, and structural deduction available.

Conclusion

It was never a question of the quality of the buildings or their desirability; it was strictly about their operational systems, which differed between Arthur and Eleanor. Arthur’s lack of accounting for rental property skills results in ongoing administrative stress and financial paralysis. Eleanor created an automated, compliant, and well-understood accounting environment, leading to financial clarity and unwavering confidence in her investments.

Your rental property portfolio is a business, and like any business, you want a solid financial base. Control your income and expense tracking, make use of special software tools, classify your costs to the T, and never pass up on the chance to use experts and specialised management accounts to watch your portfolio grow.

As your property operations expand, broader aspects such as compliance, portfolio reporting, and operational accounting become equally important — these are explored in detail in our complete guide to property management accounting.

People Also Ask:

Do I need an accountant for my rental property?

While it is legally permissible to manage your own property bookkeeping and submit your own self-assessment tax returns, it is advisable to hire a specialist property accountant as your portfolio expands. Taxation of real estate in the UK is complicated. By having a dedicated property accountant, you’re guaranteed to be up-to-date with any changes to HMRC legislation, you’ll be future-proofed for Making Tax Digital, and you’ll find that you’re able to find the more complex tax-saving opportunities that more than adequately compensate for their professional fees.

Do I need a separate bank account for my rental property?

If you operate your rental properties through a limited company structure, a separate corporate bank account is a strict legal requirement. If you operate as an individual private landlord, it is not legally mandated, but it is highly recommended. A separate property bank account prevents your personal spending from getting mixed in with your renting business, ensures you know exactly what is coming in and out of the business, and eliminates dozens of hours of bookkeeping work.

How do I calculate the rental income tax for long-term rental properties?

To calculate your rental income tax, take your gross rental income and deduct your total allowable operational expenses (such as repairs, insurance and management fees). The remaining figure is the net taxable profit. If you hold the properties personally, this profit is added to your other personal income and taxed at your marginal income tax band (20%, 40%, or 45%), with a 20% basic rate tax credit applied to your mortgage-interest costs. If held via a limited company, the profit is subject to the standard UK Corporation Tax rates.

What expenses can I deduct from my rental property taxes?

You can deduct any operational costs incurred “wholly and exclusively” for the day-to-day running of your rental business. These include:

– Letting agent commissions and property management fees

– Landlord insurance premiums (buildings, contents, rent guarantee)

– Direct property maintenance and routine repairs (e.g., servicing a boiler, fixing a roof tile)

– Utility bills and council tax (if paid by you rather than the tenant)

– Professional fees (accountants, legal fees for short-term tenancy renewals)

– Ground rents and service charges

How do I manage VAT for my Airbnb property?

In the UK, short-term holiday accommodation bookings are treated as standard-rated taxable supplies for VAT purposes, unlike traditional long-term residential lets, which are exempt. You must closely monitor your gross holiday let revenues. Once you reach a total booking figure of £90 000 within a rolling 12-month period, you will need to register for VAT, add 20% VAT to your accommodation charges, and submit regular VAT returns (and you can also reclaim VAT on the costs of running your property).

How do I track the rental income for multiple properties?

Single-sheet manual ledgers are not suitable for tracking rental income in a diverse multi-unit portfolio. You need to use cloud accounting software that can track codes, cost centers, or tag-based classes. This means that you can label every income receipt and expense payment to a specific property address and still have one source (central business) that feeds into your bank, and you have individual property metrics as well as macro-portfolio overviews.

Which accounting software is best for rental property management?

The best software suite combines a solid cloud accounting platform with customizable property management applications. The duo of Xero and QuickBooks is regarded as the most widely used and reliable accounting software for core accounting because of its automated bank feed, Making Tax Digital compliance, and OCR receipt capture integrations. When combined with specific property overlays such as Arthur Online, Hammock, or Landlord Studio, these engines deliver the ultimate all-in-one financial solution for contemporary landlords and property managers.